Chapter 2 Basic Linear Regression

Chapter Preview. This chapter considers regression in the case of only one explanatory variable. Despite this seeming simplicity, most of the deep ideas of regression can be developed in this framework. By limiting ourselves to the one variable case, we are able to express many calculations using simple algebra. This will allow us to develop our intuition about regression techniques by reinforcing it with simple demonstrations. Further, we can illustrate the relationships between two variables graphically because we are working in only two dimensions. Graphical tools prove to be important for developing a link between the data and a model.

2.1 Correlations and Least Squares

Regression is about relationships. Specifically, we will study how two variables, an \(x\) and a \(y\), are related. We want to be able to answer questions such as, if we change the level of \(x\), what will happen to the level of \(y\)? If we compare two “subjects” that appear similar except for the \(x\) measurement, how will their \(y\) measurements differ? Understanding relationships among variables is critical for quantitative management, particularly in actuarial science where uncertainty is so prevalent.

It is helpful to work with a specific example to become familiar with key concepts. Analysis of lottery sales has not been part of traditional actuarial practice but it is a growth area in which actuaries could contribute.

Example: Wisconsin Lottery Sales. State of Wisconsin lottery administrators are interested in assessing factors that affect lottery sales. Sales consists of online lottery tickets that are sold by selected retail establishments in Wisconsin. These tickets are generally priced at $1.00, so the number of tickets sold equals the lottery revenue. We analyze average lottery sales (SALES) over a forty-week period, April, 1998 through January, 1999, from fifty randomly selected areas identified by postal (ZIP) code within the state of Wisconsin.

Although many economic and demographic variables might influence sales, our first analysis focuses on population (POP) as a key determinant. Chapter 3 will show how to consider additional explanatory variables. Intuitively, it seems clear that geographic areas with more people will have higher sales. So, other things being equal, a larger \(x=POP\) means a larger \(y=SALES.\) However, the lottery is an important source of revenue for the state and we want to be as precise as possible.

A little additional notation will be useful subsequently. In this sample, there are fifty geographic areas and we use subscripts to identify each area. For example, \(y_1\) = 1,285.4 represents sales for the first area in the sample that has population \(x_1\) = 435. Call the ordered pair (\(x_1\), \(y_1\)) = (435, 1285.4) the first observation. Extending this notation, the entire sample containing fifty observations may be represented by (\(x_1\), \(y_1\)), …, (\(x_{50}\), \(y_{50}\)). The ellipses ( … ) mean that the pattern is continued until the final object is encountered. We will often speak of a generic member of the sample, referring to (\(x_i\), \(y_i\)) as the \(i\)th observation.

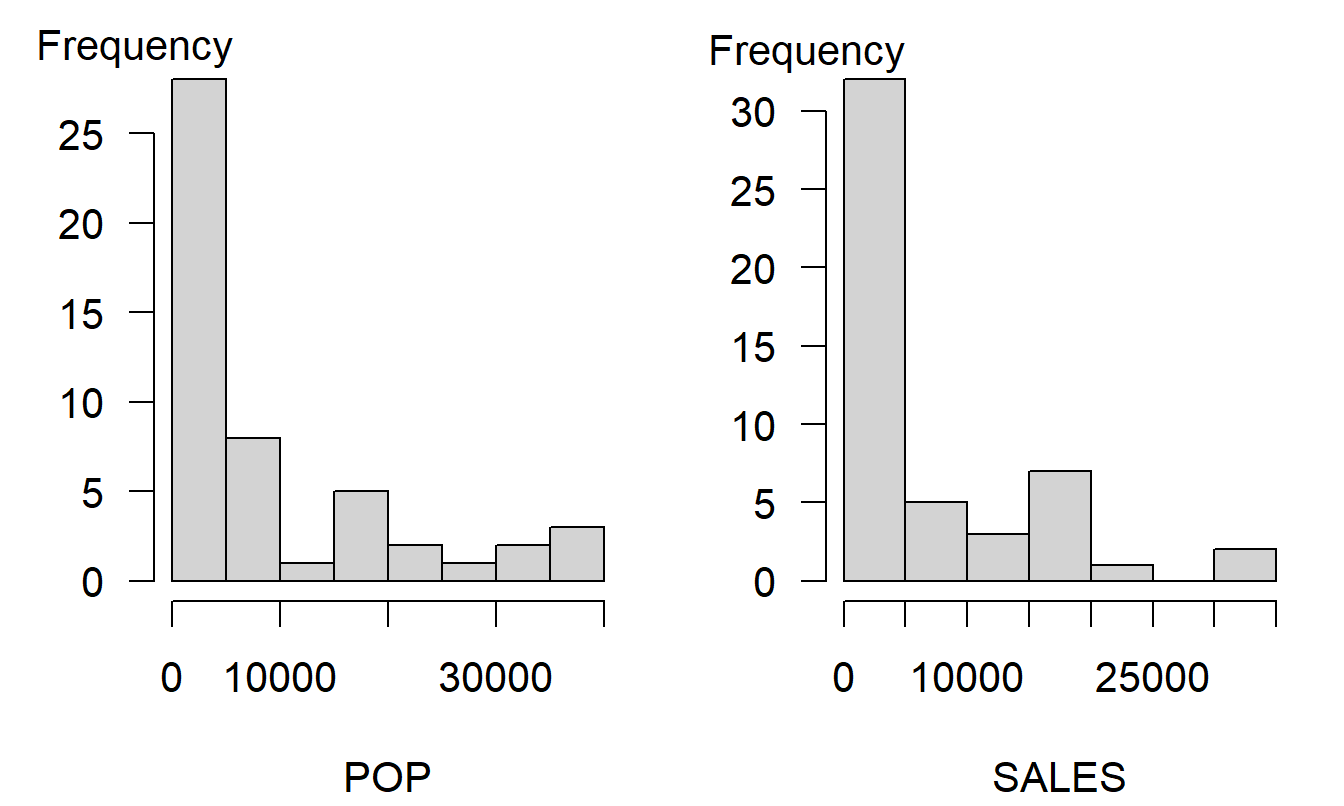

Data sets can get complicated, so it will help if you begin by working with each variable separately. The two panels in Figure 2.1 show histograms that give a quick visual impression of the distribution of each variable in isolation of the other. Table 2.1 provides corresponding numerical summaries. To illustrate, for the population variable (POP), we see that the area with the smallest number contained 280 people whereas the largest contained 39,098. The average, over 50 ZIP codes, was 9,311.04. For our second variable, sales were as low as 189 and as high as 33,181.

Figure 2.1: Histograms of Population and Sales. Each distribution is skewed to the right, indicating that there are many small areas compared to a few areas with larger sales and populations.

| Mean | Median | Standard Deviation | Minimum | Maximum | |

|---|---|---|---|---|---|

| POP | 9,311 | 4,406 | 11,098 | 280 | 39,098 |

| SALES | 6,495 | 2,426 | 8,103 | 189 | 33,181 |

| Source: Frees and Miller (2003) |

R Code to Produce Figure 2.1 and Table 2.1

As Table 2.1 shows, the basic summary statistics give useful ideas of the structure of key features of the data. After we understand the information in each variable in isolation of the other, we can begin exploring the relationship between the two variables.

Scatter Plot and Correlation Coefficients - Basic Summary Tools

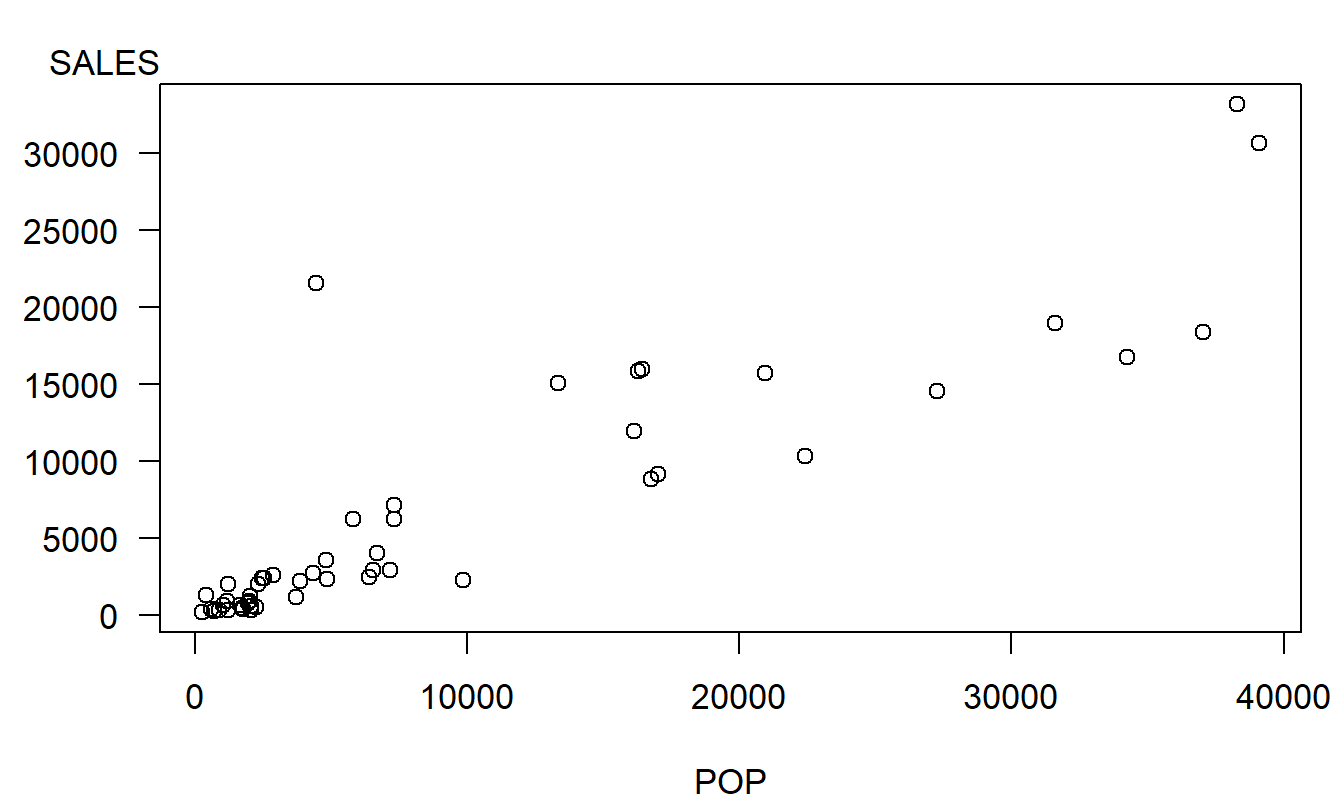

The basic graphical tool used to investigate the relationship between the two variables is a scatter plot such as in Figure 2.2. Although we may lose the exact values of the observations when graphing data, we gain a visual impression of the relationship between population and sales. From Figure 2.2 we see that areas with larger populations tend to purchase more lottery tickets. How strong is this relationship? Can knowledge of the area’s population help us anticipate the revenue from lottery sales? We explore these two questions below.

Figure 2.2: A scatter plot of the lottery data. Each of the 50 plotting symbols corresponds to a zip code in the study. This figure suggests that postal areas with larger populations have larger lottery revenues.

R Code to Produce Figure 2.2

One way to summarize the strength of the relationship between two variables is through a correlation statistic.

Definition. The ordinary, or Pearson, correlation coefficient is defined as \[ r=\frac{1}{(n-1)s_xs_y}\sum_{i=1}^{n}\left( x_{i}-\overline{x}\right) \left( y_{i}-\overline{y}\right) . \]

Here, we use the sample standard deviation \(s_y = \sqrt{(n-1)^{-1} \sum_{i=1}^{n}\left( y_i - \overline{y}\right)^{2}}\) defined in Section 1.2, with similar notation for \(s_x\).

Although there are other correlation statistics, the correlation coefficient devised by Pearson (1895) has several desirable properties. One important property is that, for any data set, \(r\) is bounded by -1 and 1, that is, \(-1\leq r\leq 1\). (Exercise 2.3 provides steps for you to check this property.) If \(r\) is greater than zero, the variables are said to be (positively) correlated. If \(r\) is less than zero, the variables are said to be negatively correlated. The larger the coefficient is in absolute value, the stronger is the relationship. In fact, if \(r=1\), then the variables are perfectly correlated. In this case, all of the data lie on a straight line that goes through the lower left and upper right-hand quadrants. If \(r=-1\), then all of the data lie on a line that goes through the upper left and lower right-hand quadrants. The coefficient \(r\) is a measure of a linear relationship between two variables.

The correlation coefficient is said to be location and scale invariant. Thus, each variable’s center of location does not matter in the calculation of \(r\). For example, if we add $100 to the sales of each zip code, each \(y_i\) will increase by 100. However, \(\overline{y}\), the average purchase price will also increase by 100 so that the deviation \(y_i - \overline{y}\) remains unchanged, or invariant. Further, the scale of each variable does not matter in the calculation of \(r\). For example, suppose we divide each population by 1000 so that \(x_i\) now represents population in thousands. Thus, \(\overline{x}\) is also divided by 1000 and you should check that \(s_x\) is also divided by 1000. Thus, the standardized version of \(x_i\), \(\left( x_i-\overline{x}\right) /s_x\), remains unchanged, or invariant. Many statistical packages compute a standardized version of a variable by subtracting the average and dividing by the standard deviation. Now, let’s use \(y_{i,std}=\left( y_i- \overline{y}\right) /s_y\) and \(x_{i,std}=\left( x_i-\overline{x} \right) /s_x\) to be the standardized versions of \(y_i\) and \(x_i\), respectively. With this notation, we can express the correlation coefficient as \(r=(n-1)^{-1}\sum_{i=1}^{n}x_{i,std}\times y_{i,std}.\)

The correlation coefficient is said to be a dimensionless measure. This is because we have taken away dollars, and all other units of measures, by considering the standardized variables \(x_{i,std}\) and \(y_{i,std}\). Because the correlation coefficient does not depend on units of measure, it is a statistic that can readily be compared across different data sets.

In the world of business, the term “correlation” is often used as synonymous with the term “relationship.” For the purposes of this text, we use the term correlation when referring only to linear relationships. The classic nonlinear relationship is \(y=x^{2}\), a quadratic relationship. Consider this relationship and the fictitious data set for \(x\), \(\{-2,1,0,1,2\}\). Now, as an exercise (2.2), produce a rough graph of the data set:

\[ \begin{array}{l|rrrrr} \hline i & 1 & 2 & 3 & 4 & 5 \\ \hline x_i & -2 & -1 & 0 & 1 & 2 \\ y_i & 4 & 1 & 0 & 1 & 4 \\ \hline \end{array} \]

The correlation coefficient for this data set turns out to be \(r=0\) (check this). Thus, despite the fact that there is a perfect relationship between \(x\) and \(y\) (\(=x^{2}\)), there is a zero correlation. Recall that location and scale changes are not relevant in correlation discussions, so we could easily change the values of \(x\) and \(y\) to be more representative of a business data set.

How strong is the relationship between \(y\) and \(x\) for the lottery data? Graphically, the response is a scatter plot, as in Figure 2.2. Numerically, the main response is the correlation coefficient which turns out to be \(r\) = 0.886 for this data set. We interpret this statistic by saying that SALES and POP are (positively) correlated. The strength of the relationship is strong because \(r\) = 0.886 is close to one. In summary, we may describe this relationship by saying that there is a strong correlation between SALES and POP.

Method of Least Squares

Now we begin to explore the question, “Can knowledge of population help us understand sales?” To respond to this question, we identify sales as the response, or dependent, variable. The population variable, which is used to help understand sales, is called the explanatory, or independent, variable.

Suppose that we have available the sample data of fifty sales \(\{y_1, \ldots, y_{50} \}\) and your job is to predict the sales of a randomly selected ZIP code. Without knowledge of the population variable, a sensible predictor is simply \(\overline{y}=6,495\), the average of the available sample. Naturally, you anticipate that areas with larger populations will have larger sales. That is, if you also have knowledge of population, then can this estimate be improved? If so, then by how much?

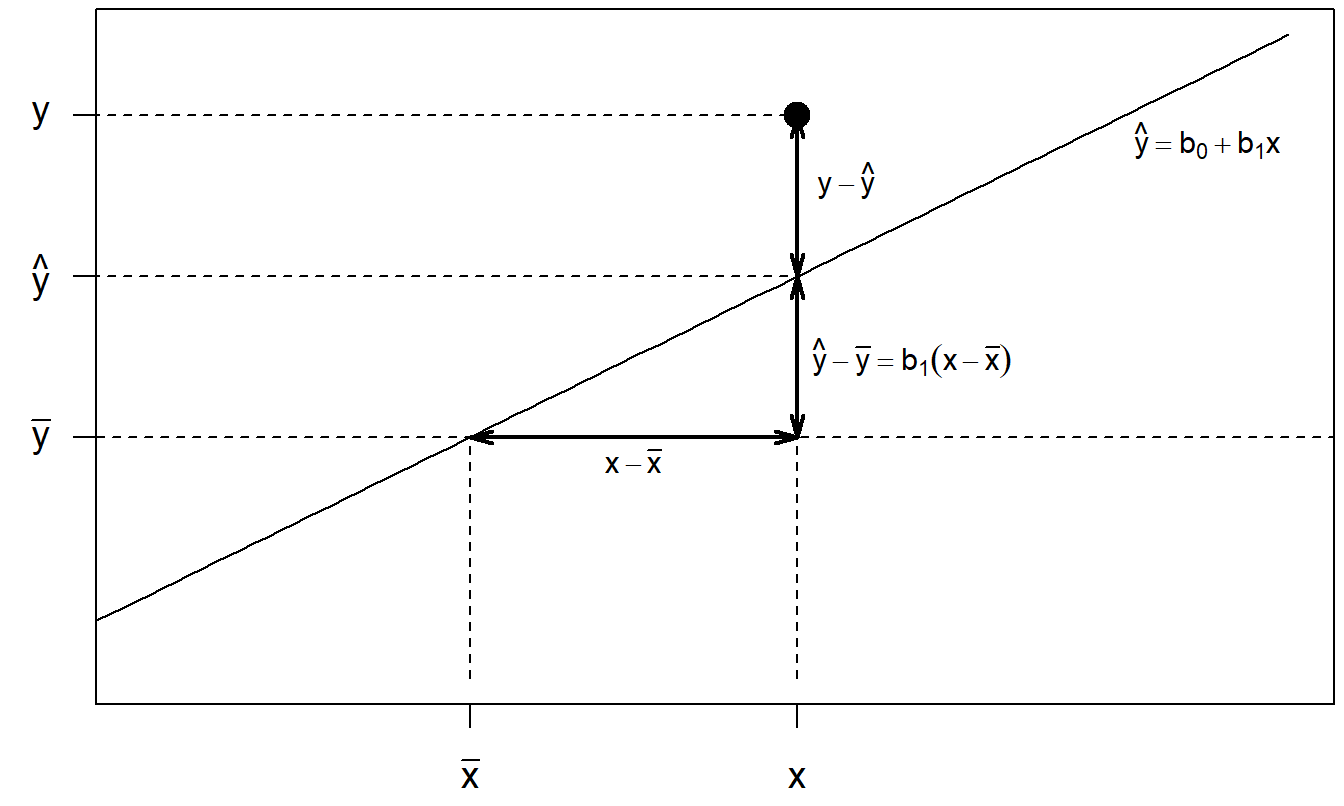

To answer these questions, the first step assumes an approximate linear relationship between \(x\) and \(y\). To fit a line to our data set, we use the method of least squares. We need a general technique so that, if different analysts agree on the data and agree on the fitting technique, then they will agree on the line. If different analysts fit a data set using eyeball approximations, in general they will arrive at different lines, even using the same data set.

The method begins with the line \(y=b_0^{\ast}+b_1^{\ast}x\), where the intercept and slope, \(b_0^{\ast}\) and \(b_1^{\ast}\), are merely generic values. For the \(i\)th observation, \(y_i-\left( b_0^{\ast}+b_1^{\ast}x_i\right)\) represents the deviation of the observed value \(y_i\) from the line at \(x_i\). The quantity \[ SS(b_0^{\ast},b_1^{\ast})=\sum_{i=1}^{n}\left( y_i-\left( b_0^{\ast}+b_1^{\ast}x_i\right) \right) ^{2} \] represents the sum of squared deviations for this candidate line. The least squares method consists of determining the values of \(b_0^{\ast}\) and \(b_1^{\ast}\) that minimize \(SS(b_0^{\ast},b_1^{\ast})\). This is an easy problem that can be solved by calculus, as follows. Taking partial derivatives with respect to each argument yields \[ \frac{\partial }{\partial b_0^{\ast}}SS(b_0^{\ast},b_1^{\ast})=\sum_{i=1}^{n}(-2)\left( y_i-\left( b_0^{\ast}+b_1^{\ast}x_i\right) \right) \] and \[ \frac{\partial }{\partial b_1^{\ast}}SS(b_0^{\ast},b_1^{\ast})=\sum_{i=1}^{n}(-2x_i)\left( y_i-\left( b_0^{\ast}+b_1^{\ast}x_i\right) \right) . \] The reader is invited to take second partial derivatives to ensure that we are minimizing, not maximizing, this function. Setting these quantities equal to zero and canceling constant terms yields \[ \sum_{i=1}^{n}\left( y_i-\left( b_0^{\ast}+b_1^{\ast}x_i\right) \right) =0 \] and \[ \sum_{i=1}^{n}x_i\left( y_i-\left( b_0^{\ast}+b_1^{\ast}x_i\right) \right) =0, \] which are known as the normal equations. Solving these equations yields the values of \(b_0^{\ast}\) and \(b_1^{\ast}\) that minimize the sum of squares, as follows.

Definition. The least squares intercept and slope estimates are

\[ b_1=r\frac{s_y}{s_x}~~~~~\mathrm{and}~~~~~b_0=\overline{y}-b_1 \overline{x}. \] The line that they determine, \(\widehat{y}=b_0+b_1x\), is called the fitted regression line.

We have dropped the asterisk, or star, notation because \(b_0\) and \(b_1\) are no longer “candidate” values.

Does this procedure yield a sensible line for our Wisconsin lottery sales? Earlier, we computed \(r=0.886\). From this and the basic summary statistics in Table 2.1, we have \(b_1 = 0.886 \left( 8,103\right) /11,098=0.647\) and \(b_0 = 6,495-(0.647)9,311 = 469.7.\) This yields the fitted regression line \[ \widehat{y} = 469.7 + (0.647)x. \] The carat, or “hat,” on top of the \(y\) reminds us that this \(\widehat{y}\), or \(\widehat{SALES}\), is a fitted value. One application of the regression line is to estimate sales for a specific population say, \(x=10,000\). The estimate is the height of the regression line, which is \(469.7 + (0.647)(10,000) = 6,939.7\).

Example: Summarizing Simulations. Regression analysis is a tool for summarizing complex data. In practical work, actuaries often simulate complicated financial scenarios; it is often overlooked that regression can be used to summarize relationships of interest.

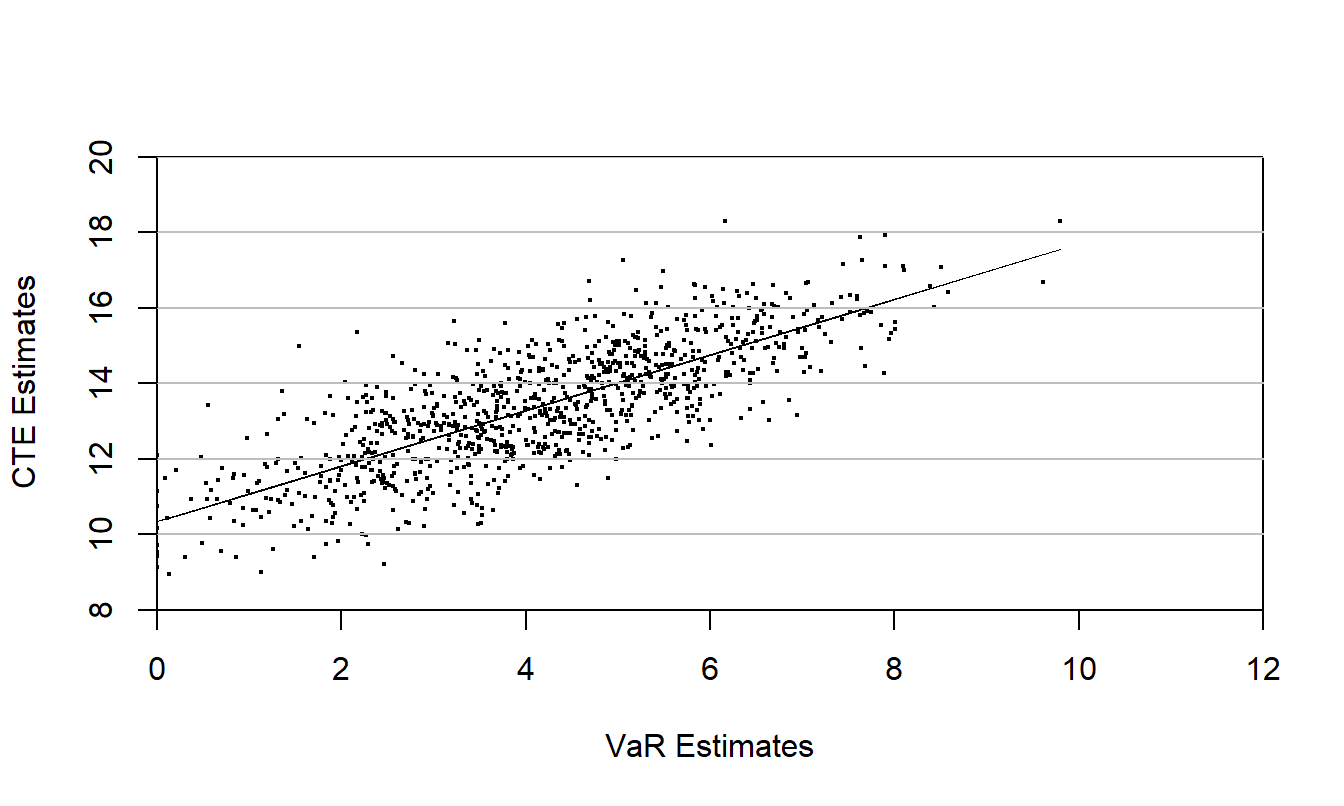

To illustrate, Manistre and Hancock (2005) simulated many realizations of a 10-year European put option and demonstrated the relationship between two actuarial risk measures, the value-at-risk (VaR) and the conditional tail expectation (CTE). For one example, these authors examined lognormally distributed stock returns with an initial stock price of $100, so that in 10 years the price of the stock would be distributed as \[ S(Z)=100 \exp \left( (.08) 10 + .15 \sqrt{10} Z \right), \] based on an annual mean return of 8%, standard deviation 15% and the outcome from a standard normal random variable \(Z\). The put option pays the difference between the strike price, that will be taken to be 110 for this example, and \(S(Z)\). The present value of this option is \[ C(Z)= \mathrm{e}^{-0.06(10)} \mathrm{max} \left(0, 110-S(Z) \right), \] based on a 6% discount rate.

To estimate the VaR and CTE, for each \(i\), 1000 i.i.d. standard normal random variables were simulated and used to calculate 1000 present values, \(C_{i1}, \ldots, C_{i,1000}.\) The 95th percentile of these present values is the estimate of the value at risk, denoted as \(VaR_i.\) The average of the highest 50 (\(= (1-.05) \times 1000\)) of the present values is the estimate of the conditional tail expectation, denoted as \(CTE_i\). Manistre and Hancock (2005) performed this calculation \(i=1, \ldots, 1000\) times; the result is presented in Figure 2.3. The scatterplot shows a strong but not perfect relationship between the \(VaR\) and the \(CTE\), the correlation coefficient turns out to be \(r=0.782\).

Figure 2.3: Plot of Conditional Tail Expectation (CTE) versus Value at Risk (VaR). Based on \(n=1,000\) simulations from a 10-year European put bond. Source: Manistre and Hancock (2005).

R Code to Produce Figure 2.3

Video: Section Summary

2.2 Basic Linear Regression Model

The scatter plot, correlation coefficient and the fitted regression line are useful devices for summarizing the relationship between two variables for a specific data set. To infer general relationships, we need models to represent outcomes of broad populations.

This chapter focuses on a “basic linear regression” model. The “linear regression” part comes from the fact that we fit a line to the data. The “basic” part is because we use only one explanatory variable, \(x\). This model is also known as a “simple” linear regression. This text avoids this language because it gives the false impression that regression ideas and interpretations with one explanatory variable are always straightforward.

We now introduce two sets of assumptions of the basic model, the “observables” and the “error” representations. They are equivalent but each will help us as we later extend regression models beyond the basics.

\[ {\small \begin{array}{l} \hline \hline &\textbf{Basic Linear Regression Model} \\ &\textbf{Observables Representation Sampling Assumptions} \\ \hline \text{F1}. & \mathrm{E}~y_i=\beta_0 + \beta_1 x_i . \\ \text{F2}. & \{x_1,\ldots ,x_n\} \text{ are non-stochastic variables}. \\ \text{F3}. & \mathrm{Var}~y_i=\sigma ^{2}. \\ \text{F4}. & \{ y_i\} \text{ are independent random variables}. \\ \hline\ \end{array} } \]

The “observables representation” focuses on variables that we can see (or observe), \((x_i,y_i)\). Inference about the distribution of \(y\) is conditional on the observed explanatory variables, so that we may treat \(\{x_1,\ldots ,x_n\}\) as non-stochastic variables (assumption F2). When considering types of sampling mechanisms for \((x_i,y_i)\), it is convenient to think of a stratified random sampling scheme, where values of \(\{x_1,\ldots ,x_n\}\) are treated as the strata, or group. Under stratified sampling, for each unique value of \(x_i\), we draw a random sample from a population. To illustrate, suppose you are drawing from a database of firms to understand stock return performance (\(y\)) and wish to stratify based on the size of the firm. If the amount of assets is a continuous variable, then we can imagine drawing a sample of size 1 for each firm. In this way, we hypothesize a distribution of stock returns conditional on firm asset size.

Digression: You will often see reports that summarize results for the “top 50 managers” or the “best 100 universities,” measured by some outcome variable. In regression applications, make sure that you do not select observations based on a dependent variable, such as the highest stock return, because this is stratifying based on the \(y\), not the \(x\). Chapter 6 will discuss sampling procedures in greater detail.

Stratified sampling also provides motivation for assumption F4, the independence among responses. One can motivate assumption F1 by thinking of \((x_i,y_i)\) as a draw from a population, where the mean of the conditional distribution of \(y_i\) given {\(x_i\)} is linear in the explanatory variable. Assumption F3 is known as homoscedasticity that we will discuss extensively in Section 5.7. See Goldberger (1991) for additional background on this representation.

A fifth assumption that is often implicitly used is:

\[ \text{F}5. ~~\{y_i\}~ \text{ are normally distributed}. \]

This assumption is not required for many statistical inference procedures because central limit theorems provide approximate normality for many statistics of interest. However, formal justification for some, such as \(t\)-statistics, do require this additional assumption.

In contrast to the observables representation, an alternative set of assumptions focuses on the deviations, or “errors,” in the regression, defined as \(\varepsilon_i=y_i-\left( \beta_0 + \beta_1 x_i \right)\).

\[ {\small \begin{array}{l} \hline \hline &\textbf{Basic Linear Regression Model} \\ &\textbf{Error Representation Sampling Assumptions} \\ \hline \text{E1}. & y_i=\beta_0 + \beta_1 x_i + \varepsilon_i . \\ \text{E2}. & \{x_1,\ldots ,x_n\} \text{ are non-stochastic variables}. \\ \text{E3}. & \mathrm{E}~\varepsilon_i=0 \text{ and } \mathrm{Var}~\varepsilon_i=\sigma ^{2}. \\ \text{E4}. & \{ \varepsilon_i\} \text{ are independent random variables}. \\ \hline\ \end{array} } \]

The “error representation” is based on the Gaussian theory of errors (see Stigler, 1986, for a historical background). Assumption E1 assumes that \(y\) is in part due to a linear function of the observed explanatory variable, \(x\). Other unobserved variables that influence the measurement of \(y\) are interpreted to be included in the “error” term \(\varepsilon_i\), which is also known as the “disturbance” term. The independence of errors, E4, can be motivated by assuming that {\(\varepsilon_i\)} are realized through a simple random sample from an unknown population of errors.

Assumptions E1-E4 are equivalent to F1-F4. The error representation provides a useful springboard for motivating goodness of fit measures (Section 2.3). However, a drawback of the error representation is that it draws the attention from the observable quantities \((x_i,y_i)\) to an unobservable quantity, {\(\varepsilon_i\)}. To illustrate, the sampling basis, viewing {\(\varepsilon_i\)} as a simple random sample, is not directly verifiable because one cannot directly observe the sample {\(\varepsilon_i\)}. Moreover, the assumption of additive errors in E1 will be troublesome when we consider nonlinear regression models.

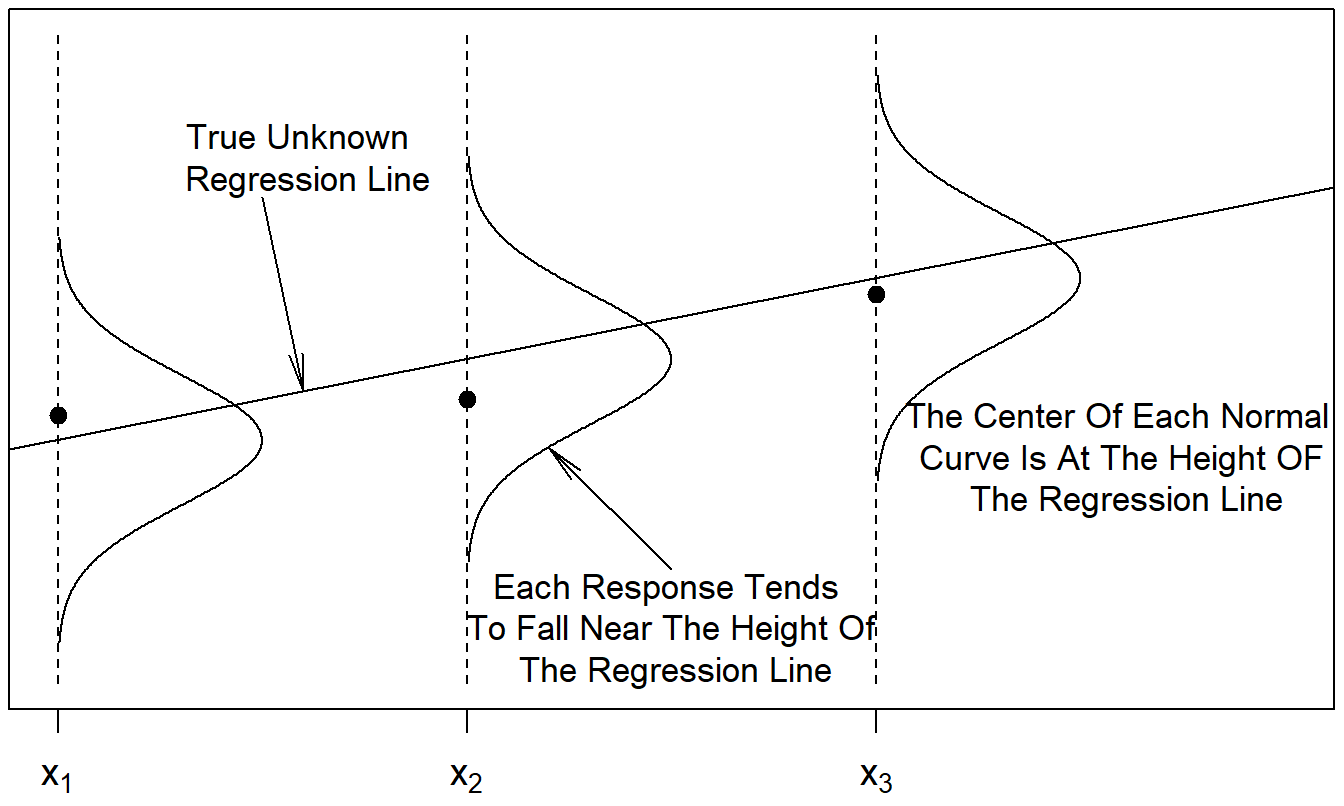

Figure 2.4 illustrates some of the assumptions of the basic linear regression model. The data (\(x_1,y_1\)), (\(x_2,y_2\)) and (\(x_3,y_3\)) are observed and are represented by the circular opaque plotting symbols. According to the model, these observations should be close to the regression line \(\mathrm{E}~y = \beta_0 + \beta_1 x\). Each deviation from the line is random. We will often assume that the distribution of deviations may be represented by a normal curve, as in Figure 2.4.

Figure 2.4: The distribution of the response varies by the level of the explanatory variable.

The basic linear regression model assumptions describe the underlying population. Table 2.2 highlights the idea that characteristics of this population can be summarized by the parameters \(\beta_0\), \(\beta_1\) and \(\sigma ^{2}\). In Section 2.1, we summarized data from a sample, introducing the statistics \(b_0\) and \(b_1\). Section 2.3 will introduce \(s^{2}\), the statistic corresponding to the parameter \(\sigma ^{2}\).

Table 2.2. Summary Measures of the Population and Sample

\[ {\small \begin{array}{llccc}\hline\hline & \text{Summary} \\ \text{Data} & \text{Measures} & \text{Intercept} & \text{Slope} & \text{Variance} \\\hline \text{Population} & \text{Parameters} & \beta_0 & \beta_1 & \sigma^2 \\ \text{sample} & \text{Statistics} & b_0 & b_1 & s^2 \\ \hline \end{array} } \]

Video: Section Summary

2.3 Is the Model Useful? Some Basic Summary Measures

Although statistics is the science of summarizing data, it is also the art of arguing with data. This section develops some of the basic tools used to justify the basic linear regression model. A scatter plot may provide strong visual evidence that \(x\) influences \(y\); developing numerical evidence will enable us to quantify the strength of the relationship. Further, numerical evidence will be useful when we consider other data sets where the graphical evidence is not compelling.

2.3.1 Partitioning the Variability

The squared deviations, \(\left( y_i-\overline{y}\right) ^2\), provide a basis for measuring the spread of the data. If we wish to estimate the \(i\)th dependent variable without knowledge of \(x\), then \(\overline{y}\) is an appropriate estimate and \(y_i- \overline{y}\) represents the deviation of the estimate. We use \(Total~SS=\sum_{i=1}^{n}\left( y_i-\overline{y}\right) ^2\), the total sum of squares, to represent the variation in all of the responses.

Suppose now that we also have knowledge of \(x\), an explanatory variable. Using the fitted regression line, for each observation we can compute the corresponding fitted value, \(\widehat{y}_i = b_0 + b_1x_i\). The fitted value is our estimate with knowledge of the explanatory variable. As before, the difference between the response and the fitted value, \(y_i- \widehat{y}_i\), represents the deviation of this estimate. We now have two “estimates” of \(y_i\), these are \(\widehat{y}_i\) and \(\overline{y}\). Presumably, if the regression line is useful, then $ _i$ is a more accurate measure than \(\overline{y}\). To judge this usefulness, we algebraically decompose the total deviation as:

\[\begin{equation} \begin{array}{ccccc} \underbrace{y_i-\overline{y}} & = & \underbrace{y_i-\widehat{y}_i} & + & \underbrace{\widehat{y}_i-\overline{y}} \\ \text{total} & = & \text{unexplained} & + & \text{explained} \\ \text{deviation} & & \text{deviation} & & \text{deviation} \\ \end{array} \tag{2.1} \end{equation}\] Interpret this equation as “the deviation without knowledge of \(x\) equals the deviation with knowledge of \(x\) plus the deviation explained by \(x\).” Figure 2.5 is a geometric display of this decomposition. In the figure, an observation above the line was chosen, yielding a positive deviation from the fitted regression line, to make the graph easier to read. A good exercise is to draw a rough sketch corresponding to Figure 2.5 with an observation below the fitted regression line.

Figure 2.5: Geometric display of the deviation decomposition.

Now, from the algebraic decomposition in equation (2.1), square each side of the equation and sum over all observations. After a little algebraic manipulation, this yields \[\begin{equation} \sum_{i=1}^{n}\left( y_i-\overline{y}\right) ^2=\sum_{i=1}^{n}\left( y_i-\widehat{y}_i\right) ^2+\sum_{i=1}^{n}\left( \widehat{y}_i- \overline{y}\right) ^2. \tag{2.2} \end{equation}\] We rewrite this as \(Total~SS=Error~SS+Regression~SS\) where \(SS\) stands for sum of squares. We interpret:

\(Total~SS\) as the total variation without knowledge of \(x\),

\(Error~SS\) as the total variation remaining after the introduction of \(x\), and

\(Regression~SS\) as the difference between the \(Total~SS\) and \(Error~SS\) , or the total variation “explained” through knowledge of \(x\).

When squaring the right-hand side of equation (2.1), we have the cross-product term \(2\left( y_i-\widehat{y}_i\right) \left( \widehat{y}_i-\overline{y}\right)\). With the “algebraic manipulation,” one can check that the sum of the cross-products over all observations is zero. This result is not true for all fitted lines but is a special property of the least squares fitted line.

In many instances, the variability decomposition is reported through only a single statistic.

Definition. The coefficient of determination is denoted by the symbol \(R^2\), called “\(R\)-square, and defined as \[ R^2=\frac{Regression~SS}{Total~SS}. \]

We interpret \(R^2\) to be the proportion of variability explained by the regression line. In one extreme case where the regression line fits the data perfectly, we have \(Error~SS=0\) and \(R^2=1\). In the other extreme case where the regression line provides no information about the response, we have \(Regression~SS=0\) and \(R^2=0.\) The coefficient of determination is constrained by the inequalities \(0 \leq R^2 \leq 1\) with larger values implying a better fit.

2.3.2 The Size of a Typical Deviation: s

In the basic linear regression model, the deviation of the response from the regression line, \(y_i-\left( \beta_0+\beta_1x_i\right)\), is not an observable quantity because the parameters \(\beta_0\) and \(\beta_1\) are not observed. However, by using estimators \(b_0\) and \(b_1\), we can approximate this deviation using \[ e_i=y_i-\widehat{y}_i=y_i-\left( b_0+b_1x_i\right) , \] known as the residual.

Residuals will be critical to developing strategies for improving model specification in Section 2.6. We now show how to use the residuals to estimate \(\sigma ^2\). From a first course in statistics, we know that if one could observe the deviations \(\varepsilon_i\), then a desirable estimate of \(\sigma ^2\) would be \((n-1)^{-1}\sum_{i=1}^{n}\left( \varepsilon _i-\overline{\varepsilon }\right) ^2\). Because {\(\varepsilon_i\)} are not observed, we use the following.

Definition. An estimator of \(\sigma ^2\), the mean square error (MSE), is defined as \[\begin{equation} s^2=\frac{1}{n-2}\sum_{i=1}^{n}e_i{}^2. \tag{2.3} \end{equation}\] The positive square root, \(s=\sqrt{s^2},\) is called the residual standard deviation.

Comparing the definitions of \(s^2\) and \((n-1)^{-1}\sum_{i=1}^{n}\left( \varepsilon_i-\overline{\varepsilon }\right) ^2\), you will see two important differences. First, in defining \(s^2\) we have not subtracted the average residual from each residual before squaring. This is because the average residual is zero, a special property of least squares estimation (see Exercise 2.14). This result can be shown using algebra and is guaranteed for all data sets.

Second, in defining \(s^2\) we have divided by \(n-2\) instead of \(n-1\). Intuitively, dividing by either \(n\) or \(n-1\) tends to underestimate \(\sigma ^2\). The reason is that, when fitting lines to data, we need at least two observations to determine a line. For example, we must have at least three observations for there to be any variability about a line. How much “freedom” is there for variability about a line? We will say that the error degrees of freedom is the number of observations available, \(n\), minus the number of observations needed to determine a line, 2 (with symbols, \(df=n-2\)). However, as we saw in the least squares estimation subsection, we do not need to identify two actual observations to determine a line. The idea is that if an analyst knows the line and \(n-2\) observations, then the remaining two observations can be determined, without variability. When dividing by \(n-2\), it can be shown that \(s^2\) is an unbiased estimator of \(\sigma ^2\).

We can also express \(s^2\) in terms of the sum of squares quantities. That is,

\[ s^2=\frac{1}{n-2}\sum_{i=1}^{n}\left( y_i-\widehat{y}_i\right) ^2= \frac{Error~SS}{n-2}=MSE. \]

This leads us to the analysis of variance, or ANOVA, table:

\[ \begin{array}{llcl} \hline \hline \text{ANOVA Table} \\ \hline \text{Source} & \text{Sum of Squares} & df & \text{Mean Square} \\ \hline \text{Regression} & Regression~SS & 1 & Regression~MS \\ \text{Error} & Error~SS & n-2 & MSE \\ \text{Total} & Total~SS & n-1 & \\ \hline \hline \end{array} \]

The ANOVA table is merely a bookkeeping device used to keep track of the sources of variability; it routinely appears in statistical software packages as part of the regression output. The mean square column figures are defined to be the sums of square (\(SS\)) figures divided by their respective degrees of freedom (\(df\)). In particular, the mean square for errors (\(MSE\)) equals \(s^2\) and the regression sum of squares equals the regression mean square. This latter property is specific to the regression with one variable case; it is not true where we consider more than one explanatory variable.

The error degrees of freedom in the ANOVA table is \(n-2\). The total degrees of freedom is \(n-1\), reflecting the fact that the total sum of squares is centered about the mean (at least two observations are required for positive variability). The single degree of freedom associated with the regression portion means that the slope, plus one observation, is enough information to determine the line. This is because it takes two observations to determine a line and at least three observations for there to be any variability about the line.

The analysis of variance table for the lottery data is:

| Sum of Squares | \(df\) | Mean Square | |

|---|---|---|---|

| Regression | 2,527,165,015 | 1 | 2,527,165,015 |

| Error | 690,116,755 | 48 | 14,377,432 |

| Total | 3,217,281,770 | 49 |

R Code to Produce Lottery ANOVA Table

From this table, you can check that \(R^2=78.5\%\) and \(s=3,792.\)

Video: Section Summary

2.4 Properties of Regression Coefficient Estimators

The least squares estimates can be expressed as weighted sum of the responses. To see this, define the weights \[ w_i=\frac{x_i-\overline{x}}{s_x^2(n-1)}. \] Because the sum of \(x\)-deviations (\(x_i-\overline{x}\)) is zero, we see that \(\sum_{i=1}^{n}w_i=0\). Thus, we can express the slope estimate \[\begin{equation} b_1=r\frac{s_y}{s_x}=\frac{1}{(n-1)s_x^2}\sum_{i=1}^{n}\left( x_i-\overline{x}\right) \left( y_i-\overline{y}\right) =\sum_{i=1}^{n}w_i\left( y_i-\overline{y}\right) =\sum_{i=1}^{n}w_iy_i. \tag{2.4} \end{equation}\]

The exercises ask the reader to verify that \(b_0\) can also be expressed as a weighted sum of responses, so our discussion pertains to both regression coefficients. Because regression coefficients are weighted sums of responses, they can be affected dramatically by unusual observations (see Section 2.6).

Because \(b_1\) is a weighted sum, it is straightforward to derive the expectation and variance of this statistic. By the linearity of expectations and Assumption F1, we have \[ \mathrm{E}~b_1=\sum_{i=1}^{n}w_i~\mathrm{E}~y_i=\beta_0\sum_{i=1}^{n}w_i+\beta_1\sum_{i=1}^{n}w_ix_i=\beta_1. \] That is, \(b_1\) is an unbiased estimator of \(\beta_1\). Here, the sum \(\sum_{i=1}^{n}w_ix_i\) \(=\) \(\left[ s_x^2(n-1)\right] ^{-1}\sum_{i=1}^{n}\left( x_i-\overline{x}\right) x_i\) \(=\left[s_x^2(n-1)\right] ^{-1}\sum_{i=1}^{n}\left( x_i-\overline{x}\right) ^2=1.\) From the definition of the weights, some easy algebra also shows that \(\sum_{i=1}^{n}w_i^2=1/\left( s_x^2(n-1)\right)\). Further, the independence of the responses implies that the variance of the sum is the sum of the variances, and thus we have \[ \mathrm{Var}~b_1 =\sum_{i=1}^{n}w_i^2\mathrm{Var}~y_i=\frac{\sigma^2}{s_x^2(n-1)}. \] Replacing \(\sigma ^2\) by its estimator \(s^2\) and taking square roots leads to the following.

Definition. The standard error of \(b_1\), the estimated standard deviation of \(b_1\), is defined as \[\begin{equation} se(b_1)=\frac{s}{s_x\sqrt{n-1}}. \tag{2.5} \end{equation}\]

This is our measure of the reliability, or precision, of the slope estimator. Using equation (2.5), we see that \(se(b_1)\) is determined by three quantities, \(n\), \(s\) and \(s_x\), as follows:

- If we have more observations so that \(n\) becomes larger, then $ se(b_1)$ becomes smaller, other things equal.

- If the observations have a greater tendency to lie closer to the line so that \(s\) becomes smaller, then \(se(b_1)\) becomes smaller, other things equal.

- If values of the explanatory variable become more spread out so that $ s_x$ increases, then \(se(b_1)\) becomes smaller, other things equal.

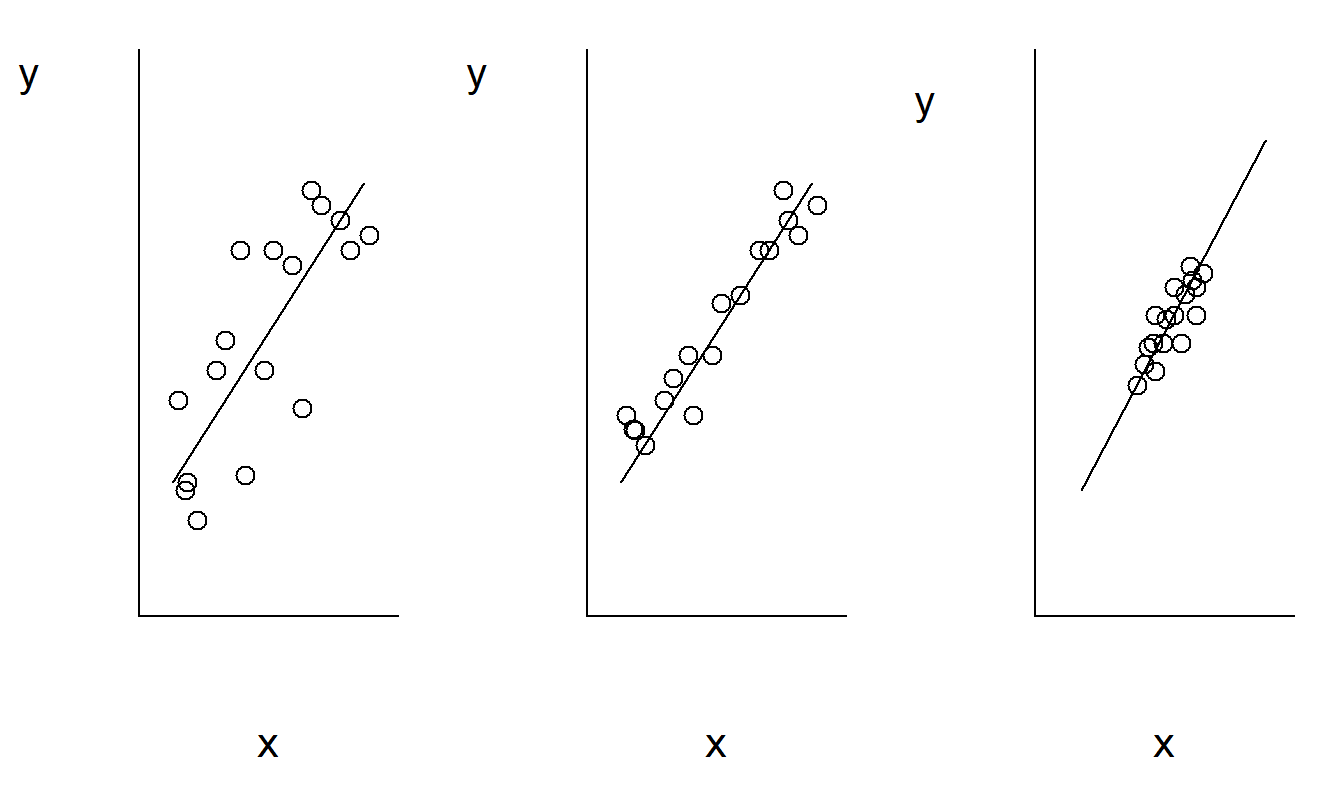

Smaller values of \(se(b_1)\) offer a better opportunity to detect relations between \(y\) and \(x\). Figure 2.6 illustrates these relationships. Here, the scatter plot in the middle has the smallest value of \(se(b_1)\). Compared with the middle plot, the left-hand plot has a larger value of \(s\) and thus \(se(b_1)\). Compared with the right-hand plot, the middle plot has a larger \(s_x\), and thus smaller value of \(se(b_1)\).

Figure 2.6: These three scatter plots exhibit the same linear relationship between \(y\) and \(x\). The plot on the left exhibits greater variability about the line than the plot in the middle. The plot on the right exhibits a smaller standard deviation in \(x\) than the plot in the middle.

R Code to Produce Figure 2.6

Equation (2.4) also implies that the regression coefficient \(b_1\) is normally distributed. That is, recall from mathematical statistics that linear combinations of normal random variables are also normal. Thus, if Assumption F5 holds, then \(b_1\) is normally distributed. Moreover, several versions of central limit theorems exists for weighted sums (see, for example, Serfling, 1980). Thus, as discussed in Section 1.4, if the responses \(y_i\) are even approximately normally distributed, then it will be reasonable to use a normal approximation for the sampling distribution of \(b_1\). Using \(se(b_1)\) as the estimated standard deviation of \(b_1\), for large values of \(n\) we have that \(\left( b_1-\beta_1\right) /se(b_1)\) has an approximate standard normal distribution. Although we will not prove it here, under Assumption F5 \(\left( b_1-\beta_1\right) /se(b_1)\) follows a $t $-distribution with degrees of freedom \(df=n-2\).

Video: Section Summary

2.5 Statistical Inference

Having fit a model with a data set, we can make a number of important statements. Generally, it is useful to think about these statements in three categories: (i) tests of hypothesized ideas, (ii) estimates of model parameters and (ii) predictions of new outcomes.

2.5.1 Is the Explanatory Variable Important?: The t-Test

We respond to the question of whether the explanatory variable is important by investigating whether or not \(\beta_1=0\). The logic is that if \(\beta_1=0\), then the basic linear regression model no longer includes an explanatory variable \(x\). Thus, we translate our question of the importance of the explanatory variable into a narrower question that can be answered using the hypothesis testing framework. This narrower question is, is \(H_0:\beta_1=0\) valid? We respond to this question by looking at the test statistic:

\[ t-\mathrm{ratio}=\frac{\mathrm{estimator-hypothesized~value~of~parameter}} {\mathrm{standard~error~of~the~estimator}}. \]

For the case of \(H_0:\beta_1=0\) , we examine \(t\)-ratio \(t(b_1)=b_1/se(b_1)\) because the hypothesized value of \(\beta_1\) is 0. This is the appropriate standardization because, under the null hypothesis and the model assumptions described in Section 2.4, the sampling distribution of \(t(b_1)\) can be shown to be the \(t\)-distribution with \(df=n-2\) degrees of freedom. Thus, to test the null hypothesis \(H_0\) against the alternative \(H_{a}:\beta_1\neq 0\), we reject \(H_0\) if favor of \(H_{a}\) if \(|t(b_1)|\) exceeds a \(t\)-value. Here, this \(t\)-value is a percentile from the \(t\)-distribution using \(df=n-2\) degrees of freedom. We denote the significance level as \(\alpha\) and this \(t\)-value as \(t_{n-2,1-\alpha /2}\).

Example: Lottery Sales - Continued. For the lottery sales example, the residual standard deviation is \(s=3,792\). From Table 2.1, we have \(s_x = 11,098\). Thus, the standard error of the slope is \(se(b_1) = 3792/(11098\sqrt{50-1})=0.0488\). From Section 2.1, the slope estimate is \(b_1=0.647\). Thus, the \(t\)-statistic is \(t(b_1) = 0.647/0.0488 = 13.4\). We interpret this by saying that the slope is 13.4 standard errors above zero. For the significance level, we use the customary value of \(\alpha\) = 5%. The 97.5th percentile from a \(t\)-distribution with \(df=50-2=48\) degrees of freedom is \(t_{48,0.975}=2.011\). Because \(|13.4|>2.011\), we reject the null hypothesis that the slope \(\beta_1 = 0\) in favor of the alternative that \(\beta_1 \neq 0\).

Making decisions by comparing a \(t\)-ratio to a \(t\)-value is called a \(t\)-test. Testing \(H_0:\beta_1=0\) versus \(H_{a}:\beta_1\neq 0\) is just one of many hypothesis tests that can be performed, although it is the most common. Table 2.3 outlines alternative decision-making procedures. These procedures are for testing \(H_0:\beta_1 = d\) where \(d\) is a user-prescribed value that may be equal to zero or any other known value. For example, in our Section 2.7 example, we will use \(d=1\) to test financial theories about the stock market.

Table 2.3 Decision-Making Procedures for Testing \(H_0:\beta_1 = d\)

\[ \begin{array}{c|c} \hline \text{Alternative Hypothesis} (H_{a}) & \text{Procedure: Reject } H_0 \text{ in favor of } H_{a} \text{ if} \\ \hline \beta_1>d & t-\mathrm{ratio}>t_{n-2,1-\alpha }. \\ \beta_1<d & t-\mathrm{ratio}<-t_{n-2,1-\alpha }. \\ \beta_1\neq d & |t-\mathrm{ratio}\mathit{|}>t_{n-2,1-\alpha /2}. \\ \end{array} \\ {\small \begin{array}{l} \hline \text{Notes: The significance level is } \alpha . \text{Here, }t_{n-2,1-\alpha} \text{ the } (1-\alpha )th \text{ percentile}\\ ~~\text{from the } t-\text{distribution using } df=n-2 \text{ degrees of freedom}.\\ ~~\text{The test statistic is }t-\mathrm{ratio} = (b_1 -d)/se(b_1) . \\ \hline \end{array} } \]

Alternatively, one can construct probability (\(p\)-) values and compare these to given significant levels. The \(p\)-value is a useful summary statistic for the data analyst to report since it allows the report reader to understand the strength of the deviation from the null hypothesis. Table 2.4 summarizes the procedure for calculating \(p\)-values.

Table 2.4 Probability Values for Testing \(H_0:\beta_1 = d\)

\[ \begin{array}{c|ccc} \hline \text{Alternative} & & & \\ \text{Hypothesis} (H_a) & \beta_1>d & \beta_1<d & \beta_1\neq d \\ \hline p-value & \Pr(t_{n-2}>t-\mathrm{ratio}) & \Pr(t_{n-2}<t-\mathrm{ratio}) & \Pr (|t_{n-2}|>|t-\mathrm{ratio}\mathit{|}) \\\hline \end{array} \\ {\small \begin{array}{l} \hline \text{Notes: Here, }t_{n-2} \text{ is a } t-\text{distributed random variable with } df=n-2 \text{ degrees of freedom.}\\ ~~\text{The test statistic is }t-\mathrm{ratio} = (b_1 -d)/se(b_1) . \\ \hline \end{array} } \]

Another interesting way of addressing the question of the importance of an explanatory variable is through the correlation coefficient. Remember that the correlation coefficient is a measure of linear relationship between \(x\) and \(y\). Let’s denote this statistic by \(r(y,x)\). This quantity is unaffected by scale changes in either variable. For example, if we multiply the \(x\) variable by the number \(b_1\), then the correlation coefficient remains unchanged. Further, correlations are unchanged by additive shifts. Thus, if we add a number, say \(b_0\), to each \(x\) variable, then the correlation coefficient remains unchanged. Using a scale change and an additive shift on the \(x\) variable can be used to produce the fitted value \(\widehat{y}=b_0+b_1x\). Thus, using notation, we have \(|r(y,x)|=r(y,\widehat{y}).\) We may thus interpret the correlation between the responses and the explanatory variable to be equal to the correlation between the responses and the fitted values. This leads then to the following interesting algebraic fact, \(R^2=r^2.\) That is, the coefficient of determination equals the correlation coefficient squared. This is much easier to interpret if one thinks of \(r\) as the correlation between observed and fitted values. See Exercise 2.13 for steps useful in confirming this result.

2.5.2 Confidence Intervals

Investigators often cite the formal hypothesis testing mechanism to respond to the question “Does the explanatory variable have a real influence on the response?” A natural follow-up question is “To what extent does \(x\) affect \(y\)?” To a certain degree, one could respond using the size of the \(t\)-ratio or the \(p\)-value. However, in many instances a confidence interval for the slope is more useful.

To introduce confidence intervals for the slope, recall that \(b_1\) is our point estimator of the true, unknown slope \(\beta_1\). Section 2.4 argued that this estimator has standard error \(se(b_1)\) and that \(\left( b_1-\beta_1\right) /se(b_1)\) follows a \(t\)-distribution with \(n-2\) degrees of freedom. Probability statements can be inverted to yield confidence intervals. Using this logic, we have the following confidence interval for the slope \(\beta_1\).

Definition. A \(100(1-\alpha)\)% confidence interval for the slope \(\beta_1\) is \[\begin{equation} b_1\pm t_{n-2,1-\alpha /2} ~se(b_1). \tag{2.6} \end{equation}\]

As with hypothesis testing, \(t_{n-2,1-\alpha /2}\) is the (1-\(\alpha\)/2)th percentile from the \(t\)-distribution with \(df=n-2\) degrees of freedom. Because of the two-sided nature of confidence intervals, the percentile is 1 - (1 - confidence level) / 2. In this text, for notational simplicity we generally use a 95% confidence interval, so the percentile is 1-(1-0.95)/2 = 0.975. The confidence interval provides a range of reliability that measures the usefulness of the estimate.

In Section 2.1, we established that the least squares slope estimate for the lottery sales example is \(b_1=0.647\). The interpretation is that if a zip code’s population differs by 1,000, then we expect mean lottery sales to differ by $647. How reliable is this estimate? It turns out that \(se(b_1)=0.0488\) and thus an approximate 95% confidence interval for the slope is \[ 0.647\pm (2.011)(.0488), \] or (0.549, 0.745). Similarly, if population differs by 1,000, a 95% confidence interval for the expected change in sales is (549, 745). Here, we use the \(t\)-value \(t_{48,0.975}=2.011\) because there are 48 (= \(n\)-2) degrees of freedom and, for a 95% confidence interval, we need the 97.5th percentile.

2.5.3 Prediction Intervals

In Section 2.1, we showed how to use least squares estimators to predict the lottery sales for a zip code, outside of our sample, having a population of 10,000. Because prediction is such an important task for actuaries, we formalize the procedure so that it can be used on a regular basis.

To predict an additional observation, we assume that the level of explanatory variable is known and is denoted by \(x_{\ast}\). For example, in our previous lottery sales example we used \(x_{\ast} = 10,000\). We also assume that the additional observation follows the same linear regression model as the observations in the sample.

Using our least square estimators, our point prediction is \(\widehat{y}_{\ast} = b_0 + b_1 x_{\ast}\), the height of the fitted regression line at \(x_{\ast}\) We may decompose the prediction error into two parts:

\[ \begin{array}{ccccc} \underbrace{y_{\ast} - \widehat{y}_{\ast}} & = & \underbrace{\beta_0 - b_0 + \left( \beta_1 - b_1 \right) x_{\ast}} & + & \underbrace{\varepsilon_{\ast}} \\ {\small \text{prediction error} }& {\small =} & {\small \text{error in estimating the } }& {\small +} & {\small \text{deviation of the additional } }\\ & & {\small \text{regression line at }x}_{\ast} & & {\small \text{response from its mean}} \end{array} \]

It can be shown that the standard error of the prediction is \[ se(pred) = s \sqrt{1+\frac{1}{n}+\frac{\left( x_{\ast}-\overline{x}\right) ^2}{(n-1)s_x^2}}. \] As with \(se(b_1)\), the terms \(n^{-1}\) and \(\left( x_{\ast}-\overline{x} \right) ^2/\left[ (n-1)s_x^2\right]\) become close to zero as the sample size \(n\) becomes large. Thus, for large \(n\), we have that \(se(pred)\approx s\), reflecting that the error in estimating the regression line at a point becomes negligible and deviation of the additional response from its mean becomes the entire source of uncertainty.

Definition. A \(100(1-\alpha)\)% prediction interval at \(x_{\ast}\) is \[\begin{equation} \widehat{y}_{\ast} \pm t_{n-2,1-\alpha /2} ~se(pred) \tag{2.7} \end{equation}\] where the \(t\)-value \(t_{n-2,1-\alpha /2}\) is the same as used for hypothesis testing and the confidence interval.

For example, the point prediction at \(x_{\ast} = 10,000\) is \(\widehat{y}_{\ast}\)= 469.7 + 0.647 (10000) = 6,939.7. The standard error of this prediction is \[ se(pred) = 3,792 \sqrt{1+\frac{1}{50} + \frac{\left( 10,000-9,311\right)^2}{(50-1)(11,098)^2}} = 3,829.6. \] With a \(t\)-value equal to 2.011, this yields an approximate 95% prediction interval \[ 6,939.7 \pm (2.011)(3,829.6) = 6,939.7 \pm 7,701.3 = (-761.6, ~14,641.0). \] We interpret these results by first pointing out that our best estimate of lottery sales for a zip code with a population of 10,000 is 6,939.70. Our 95% prediction interval represents a range of reliability for this prediction. If we could see many zip codes, each with a population of 10,000, on average we expect about 19 out of 20, or 95%, would have lottery sales between 0 and 14,641. It is customary to truncate the lower bound of the prediction interval to zero if negative values of the response are deemed to be inappropriate.

R Code to Produce Section 2.5 Analyses

Video: Section Summary

2.6 Building a Better Model: Residual Analysis

Quantitative disciplines calibrate models with data. Statistics takes this one step further, using discrepancies between the assumptions and the data to improve model specification. We will examine the Section 2.2 modeling assumptions in light of the data and use any mismatch to specify a better model; this process is known as diagnostic checking (like when you go to a doctor and he or she performs diagnostic routines to check your health).

We will begin with the Section 2.2 error representation. Under this set of assumptions, the deviations {\(\varepsilon_i\)} are identically and independently distributed (i.i.d), and under assumption F5, normally distributed. To assess the validity of these assumptions, one uses (observed) residuals {\(e_i\)} as approximations for the (unobserved) deviations {\(\varepsilon_i\)}. The basic theme is that if the residuals are related to a variable or display any other recognizable pattern, then we should be able to take advantage of this information and improve our model specification. The residuals should contain little or no information and represent only natural variation from the sampling that cannot be attributed to any specific source. Residual analysis is the exercise of checking the residuals for patterns.

There are five types of model discrepancies that analysts commonly look for. If detected, the discrepancies can be corrected with the appropriate adjustments in the model specification.

Model Misspecification Issues

Lack of Independence. There may exist relationships among the deviations {\(\varepsilon_i\)} so that they are not independent.

Heteroscedasticity. Assumption E3 that indicates that all observations have a common (although unknown) variability, known as homoscedasticity. Heteroscedascity is the term used when the variability varies by observation.

Relationships between Model Deviations and Explanatory Variables. If an explanatory variable has the ability to help explain the deviation \(\varepsilon\), then one should be able to use this information to better predict \(y\).

Nonnormal Distributions. If the distribution of the deviation represents a serious departure from normality, then the usual inference procedures are no longer valid.

Unusual Points. Individual observations may have a large effect on the regression model fit, meaning that the results may be sensitive to the impact of a single observation. \end{enumerate}

This list will serve the reader throughout your study of regression analysis. Of course, with only an introduction to basic models we have not yet seen alternative models that might be used when we encounter these model discrepancies. In this book’s Part II on time series models, we will study lack of independence among data ordered over time. Chapter 5 will consider heteroscedasticity in further detail. The introduction to multiple linear regression in Chapter 3 will be our first look at handling relationships between {\(\varepsilon_i\)} and additional explanatory variables. We have, however, already had an introduction to the effect of normal distributions, seeing that \(qq\) plots can detect non-normality and that transformations can help induce approximate normality. In this section, we discuss the effects of unusual points.

Much of residual analysis is done by examining a standardized residual, a residual divided by its standard error. An approximate standard error of the residual is \(s\); in Chapter 3 we will give a precise mathematical definition. There are two reasons why we often examine standardized residuals in lieu of basic residuals. First, if responses are normally distributed, then standardized residuals are approximately realizations from a standard normal distribution. This provides a reference distribution to compare values of standardized residuals. For example, if a standardized residual exceeds two in absolute value, this is considered unusually large and the observation is called an outlier. Second, because standardized residuals are dimensionless, we get carryover of experience from one data set to another. This is true regardless of whether or not the normal reference distribution is applicable.

Outliers and High Leverage Points

Another important part of residual analysis is the identification of unusual observations in a data set. Because regression estimates are weighted averages with weights that vary by observation, some observations are more important than others. This weighting is more important than many users of regression analysis realize. In fact, the example below demonstrates that a single observation can have a dramatic effect in a large data set.

There are two directions in which a data point can be unusual, the horizontal and vertical directions. By “unusual,” we mean that an observation under consideration seems to be far from the majority of the data set. An observation that is unusual in the vertical direction is called an outlier. An observation that is unusual in the horizontal directional is called a high leverage point. An observation may be both an outlier and a high leverage point.

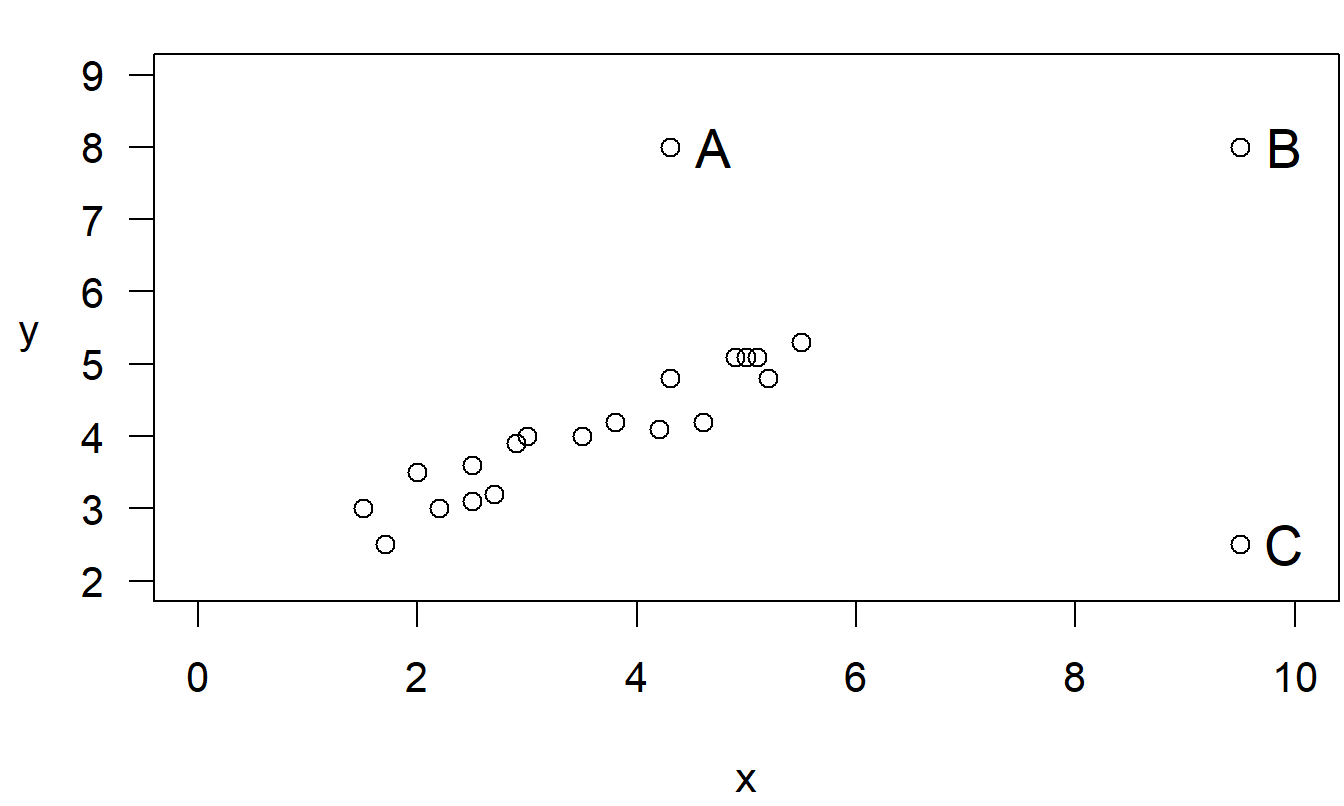

Example: Outliers and High Leverage Points. Consider the fictitious data set of 19 points plus three points, labeled A, B, and C, given in Figure 2.7 and Table 2.5. Think of the first 19 points as “good” observations that represent some type of phenomena. We want to investigate the effect of adding a single aberrant point.

Table 2.5. 19 Base Points Plus Three Types of Unusual Observations

\[ \small{ \begin{array}{c|cccccccccc|ccc} \hline Variables & &&&&&&&&& & A & B & C \\ \hline x & 1.5 & 1.7 & 2.0 & 2.2 & 2.5 & 2.5 & 2.7 & 2.9 & 3.0 & 3.5 & 3.4 & 9.5 & 9.5 \\ y & 3.0 & 2.5 & 3.5 & 3.0 & 3.1 & 3.6 & 3.2 & 3.9 & 4.0 & 4.0 & 8.0 & 8.0 & 2.5 \\ \hline x & 3.8 & 4.2 & 4.3 & 4.6 & 4.0 & 5.1 & 5.1 & 5.2 & 5.5 & & & & \\ y & 4.2 & 4.1 & 4.8 & 4.2 & 5.1 & 5.1 & 5.1 & 4.8 & 5.3 & & & & \\ \hline \end{array} } \]

Figure 2.7: Scatterplot of 19 base plus three unusual points, labeled A, B and C.

R Code to Produce Figure 2.7

To investigate the effect of each type of aberrant point, Table 2.6 summarizes the results of four separate regressions. The first regression is for the nineteen base points. The other three regressions use the nineteen base points plus each type of unusual observation.

Table 2.6. Results from Four Regressions

\[ \begin{array}{l|rrrrr} \hline Data & b_0 & b_1 & s & R^2(\%) & t(b_1) \\ \hline 19 \text{ Base Points} & 1.869 & 0.611 & 0.288 & 89.0 & 11.71 \\ 19 \text{ Base Points} ~+~ A & 1.750 & 0.693 & 0.846 & 53.7 & 4.57 \\ 19 \text{ Base Points} ~+~ B & 1.775 & 0.640 & 0.285 & 94.7 & 18.01 \\ 19 \text{ Base Points} ~+~ C & 3.356 & 0.155 & 0.865 & 10.3 & 1.44 \\ \hline \end{array} \]

Table 2.6 shows that a regression line provides a good fit for the nineteen base points. The coefficient of determination, \(R^2\), indicates about 89% of the variability has been explained by the line. The size of the typical error, \(s\), is about 0.29, small compared to the scatter in the \(y\)-values. Further, the \(t\)-ratio for the slope coefficient is large.

When the outlier point A is added to the nineteen base points, the situation deteriorates dramatically. The \(R^2\) drops from 89% to 53.7% and \(s\) increases from about 0.29 to about 0.85. The fitted regression line itself does not change that much even though our confidence in the estimates has decreased.

An outlier is unusual in the \(y\)-value, but “unusual in the \(y\)-value” depends on the \(x\)-value. To see this, keep the \(y\)-value of Point A the same, but increase the \(x\)-value and call the point B.

When the point B is added to the nineteen base points, the regression line provides a better fit. Point B is close to being on the line of the regression fit generated by the nineteen base points. Thus, the fitted regression line and the size of the typical error, \(s\), do not change much. However, \(R^2\) increases from 89% to nearly 95 percent. If we think of \(R^2\) as \(1-(Error~SS)/(Total~SS)\), by adding point B we have increased $ Total~SS$, the total squared deviations in the \(y\)’s, even though leaving \(Error~SS\) relatively unchanged. Point B is not an outlier, but it is a high leverage point.

To show how influential this point is, drop the \(y\)-value considerably and call this the new point C. When this point is added to the nineteen base points, the situation deteriorates dramatically. The \(R^2\) coefficient drops from 89% to 10%, and the \(s\) more than triples, from 0.29 to 0.87. Further, the regression line coefficients change dramatically.

Most users of regression at first do not believe that one point in twenty can have such a dramatic effect on the regression fit. The fit of a regression line can always be improved by removing an outlier. If the point is a high leverage point and not an outlier, it is not clear whether the fit will be improved when the point is removed.

Simply because you can dramatically improve a regression fit by omitting an observation does not mean you should always do so! The goal of data analysis is to understand the information in the data. Throughout the text, we will encounter many data sets where the unusual points provide some of the most interesting information about the data. The goal of this subsection is to recognize the effects of unusual points; Chapter 5 will provide options for handling unusual points in your analysis.

All quantitative disciplines, such as accounting, economics, linear programming, and so on, practice the art of sensitivity analysis. Sensitivity analysis is a description of the global changes in a system due to a small local change in an element of the system. Examining the effects of individual observations on the regression fit is a type of sensitivity analysis.

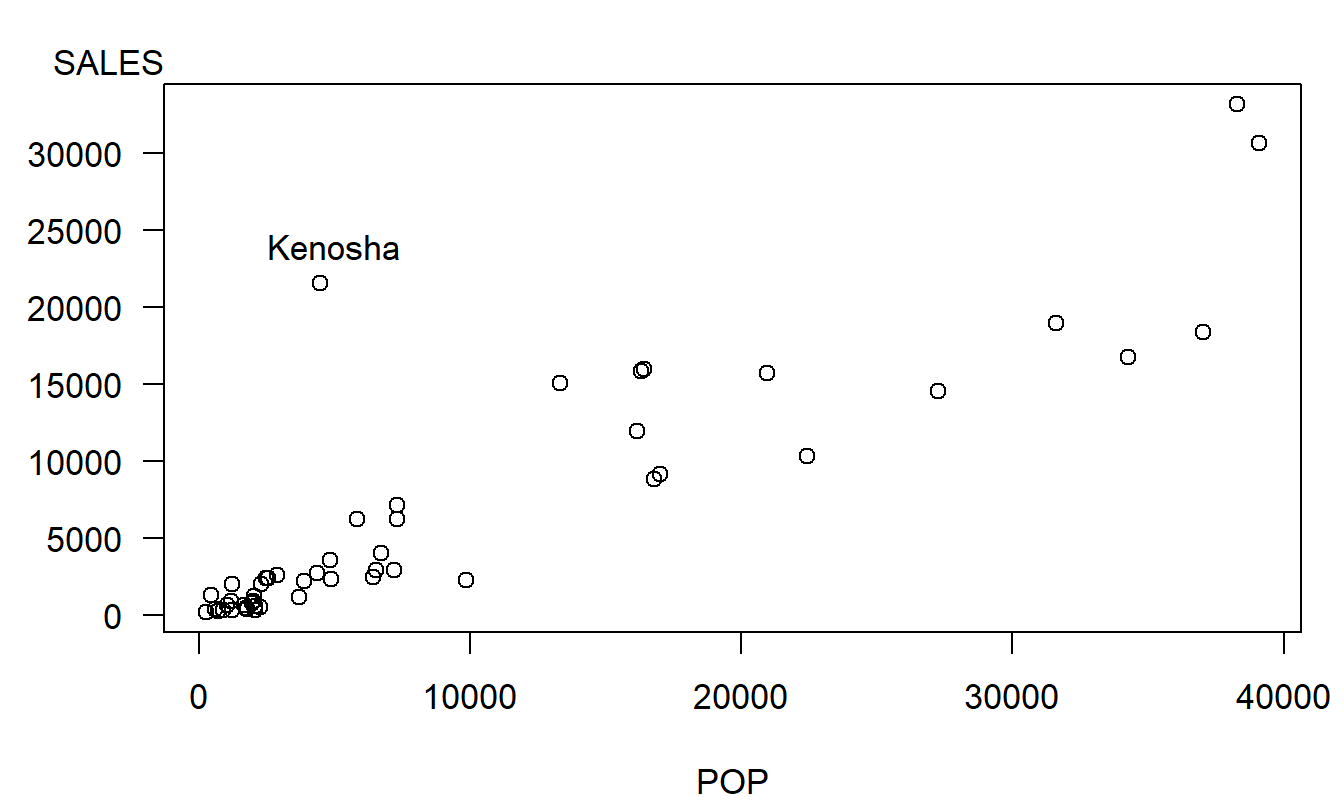

Example: Lottery Sales – Continued. Figure 2.8 exhibits an outlier; the point in the upper left-hand side of the plot represents a zip code that includes Kenosha, Wisconsin. Sales for this zip code are unusually high given its population. Kenosha is close to the Illinois border; residents from Illinois probably participate in the Wisconsin lottery thus effectively increasing the potential pool of sales in Kenosha. Table 2.7 summarizes the regression fit both with and without this zip code.

Table 2.7. Regression Results with and without Kenosha

\[ \small{ \begin{array}{l|rrrrr} \hline \text{Data} & b_0 & b_1 & s & R^2(\%) & t(b_1) \\ \hline \text{With Kenosha} & 469.7 & 0.647 & 3,792 & 78.5 & 13.26 \\ \text{Without Kenosha} & -43.5 & 0.662 & 2,728 & 88.3 & 18.82 \\ \hline \end{array} } \]

Figure 2.8: Scatter plot of SALES versus POP, with the outlier corresponding to Kenosha marked.

R Code to Produce Figure 2.8 and Table 2.7

For the purposes of inference about the slope, the presence of Kenosha does not alter the results dramatically. Both slope estimates are qualitatively similar and the corresponding \(t\)-statistics are very high, well above cut-offs for statistical significance. However, there are dramatic differences when assessing the quality of the fit. The coefficient of determination, \(R^2\), increased from 78.5% to 88.3% when deleting Kenosha. Moreover, our “typical deviation” \(s\) dropped by over $1,000. This is particularly important if we wish to tighten our prediction intervals.

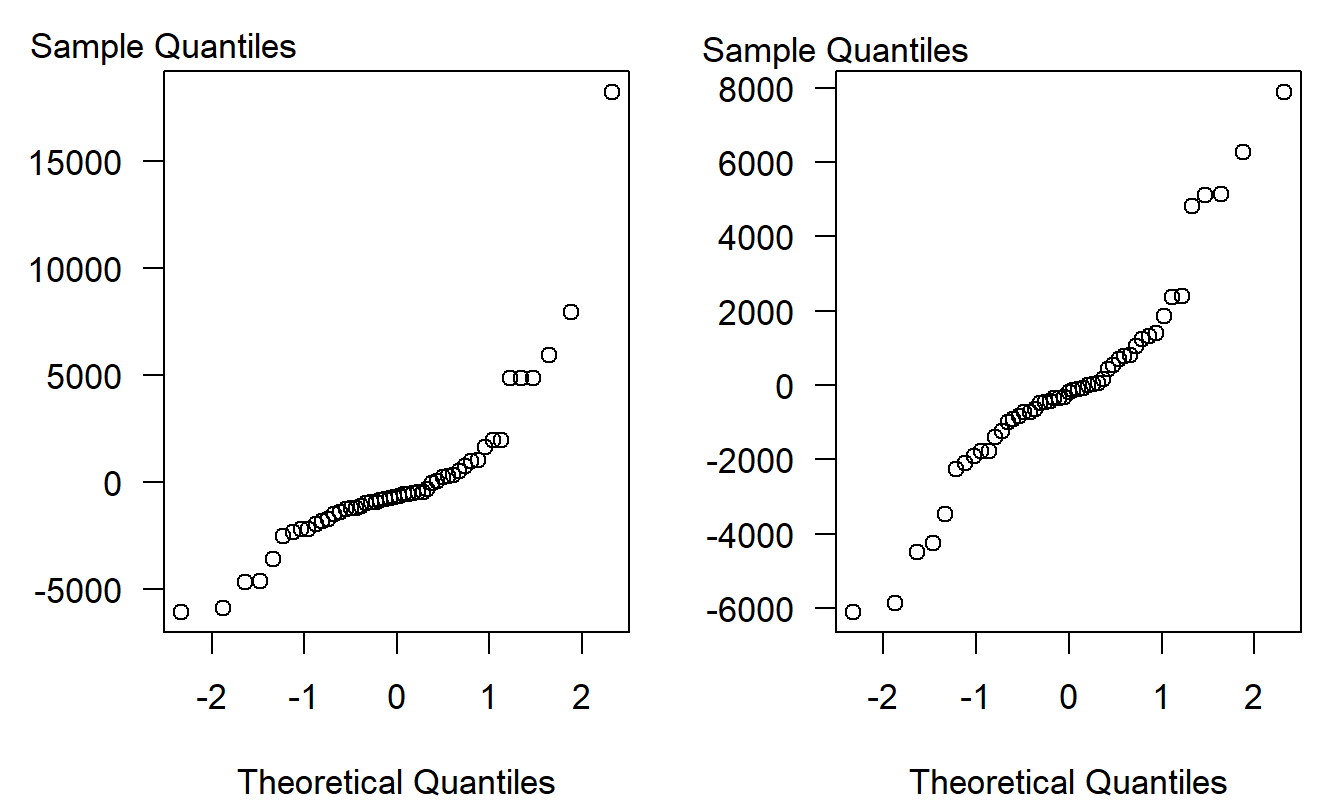

To check the accuracy of our assumptions, it is also customary to check the normality assumption. One way of doing this is the \(qq\) plot, introduced in Section 1.2. The two panels in Figures 2.9 are \(qq\) plots with and without the Kenosha zip code. Recall that points “close” to linear indicate approximate normality. In the right-hand panel of Figure 2.9, the sequence does appear to be linear so that residuals are approximately normally distributed. This is not the case in the left-hand panel, where the sequence of points appears to climb dramatically for large quantiles. The interesting thing is that the non-normality of the distribution is due to a single outlier, not a pattern of skewness that is common to all the observations.

Figure 2.9: \(qq\) Plots of Wisconsin Lottery Residuals. The left-hand panel is based on all 50 points. The right-hand panel is based on 49 points, residuals from a regression after removing Kenosha.

R Code to Produce Figure 2.9

Video: Section Summary

2.7 Application: Capital Asset Pricing Model

In this section, we study a financial application, the Capital Asset Pricing Model, often referred to by the acronym CAPM. The name is something of a misnomer in that the model is really about returns based on capital assets, not the prices themselves. The types of assets that we examine are equity securities that are traded on an active market, such as the New York Stock Exchange (NYSE). For a stock on the exchange, we can relate returns to prices through the following expression:

\[ \small{ \mathrm{return=}\frac{\mathrm{ price~at~the~end~of~a~period+dividends-price~at~the~beginning~of~a~period}}{ \mathrm{price~at~the~beginning~of~a~period}}. } \]

If we can estimate the returns that a stock generates, then knowledge of the price at the beginning of a generic financial period allows us to estimate the value at the end of the period (ending price plus dividends). Thus, we follow standard practice and model returns of a security.

An intuitively appealing idea, and one of the basic characteristics of the CAPM, is that there should be a relationship between the performance of a security and the market. One rationale is simply that if economic forces are such that the market improves, then those same forces should act upon an individual stock, suggesting that it also improve. As noted above, we measure performance of a security through the return. To measure performance of the market, several market indices exist that summarize the performance of each exchange. We will use the “equally-weighted” index of the Standard & Poor’s 500. The Standard & Poor’s 500 is the collection of the 500 largest companies traded on the NYSE, where “large” is identified by Standard & Poor’s, a financial services rating organization. The equally-weighted index is defined by assuming a portfolio is created by investing one dollar in each of the 500 companies.

Another rationale for a relationship between security and market returns comes from financial economics theory. This is the CAPM theory, attributed to Sharpe (1964) and Lintner (1965) and based on the portfolio diversification ideas of Harry Markowitz (1959). Other things equal, investors would like to select a return with a high expected value and low standard deviation, the latter being a measure of risk. One of the desirable properties about using standard deviations as a measure of riskiness is that it is straight-forward to calculate the standard deviation of a portfolio. One only needs to know the standard deviation of each security and the correlations among securities. A notable security is a risk-free one, that is, a security that theoretically has a zero standard deviation. Investors often use a 30-day U.S. Treasury bill as an approximation of a risk-free security, arguing that the probability of default of the U.S. government within 30 days is negligible. Positing the existence of a risk-free asset and some other mild conditions, under the CAPM theory there exists an efficient frontier called the securities market line. This frontier specifies the minimum expected return that investors should demand for a specified level of risk. To estimate this line, we can use the equation \[ \mathrm{E}~r = \beta_0 + \beta_1 r_m \] where \(r\) is the security return and \(r_m\) is the market return. We interpret \(\beta_1 r_m\) as a measure of the amount of security return that is attributed to the behavior of the market.

Testing economic theory, or models arising from any discipline, involves collecting data. The CAPM theory is about ex-ante (before the fact) returns even though we can only test with ex-post (after the fact) returns. Before the fact, the returns are unknown and there is an entire distribution of returns. After the fact, there is only a single realization of the security and market return. Because at least two observations are required to determine a line, CAPM models are estimated using security and market data gathered over time. In this way, several observations can be made. For the purposes of our discussions, we follow standard practice in the securities industry and examine monthly prices.

Data

To illustrate, consider monthly returns over the five year period from January, 1986 to December, 1990, inclusive. Specifically, we use the security returns from the Lincoln National Insurance Corporation as the dependent variable (\(y\)) and the market returns from the index of the Standard & Poor’s 500 Index as the explanatory variable (\(x\)). At the time, the Lincoln was a large, multi-line, insurance company, headquartered in the midwest of the U.S., specifically in Fort Wayne, Indiana. Because it was well known for its’ prudent management and stability, it is a good company to begin our analysis of the relationship between the market and an individual stock.

We begin by interpreting some basic summary statistics, in Table 2.8, in terms of financial theory. First, an investor in the Lincoln will be concerned that the five year average return, \(\overline{y}=0.00510\), is below the return of the market, \(\overline{x}=0.00741\). Students of interest theory recognize that monthly returns can be converted to an annual basis using geometric compounding. For example, the annual return of the Lincoln is \((1.0051)^{12}-1=0.062946\), or roughly 6.29 percent. This is compared to an annual return of 9.26% (= (1\(00((1.00741)^{12}-1\))) for the market. A measure of risk, or volatility, that is used in finance is the standard deviation. Thus, interpret \(s_y\) = 0.0859 \(>\) 0.05254 = \(s_x\) to mean that an investment in the Lincoln is riskier than that of the market. Another interesting aspect of Table 2.8 is that the smallest market return, -0.22052, is 4.338 standard deviations below its average ((-0.22052-0.00741)/0.05254 = -4.338). This is highly unusual with respect to a normal distribution.

| Mean | Median | Standard Deviation | Minimum | Maximum | |

|---|---|---|---|---|---|

| LINCOLN | 0.0051 | 0.0075 | 0.0859 | -0.2803 | 0.3147 |

| MARKET | 0.0074 | 0.0142 | 0.0525 | -0.2205 | 0.1275 |

| Source: Center for Research on Security Prices, University of Chicago |

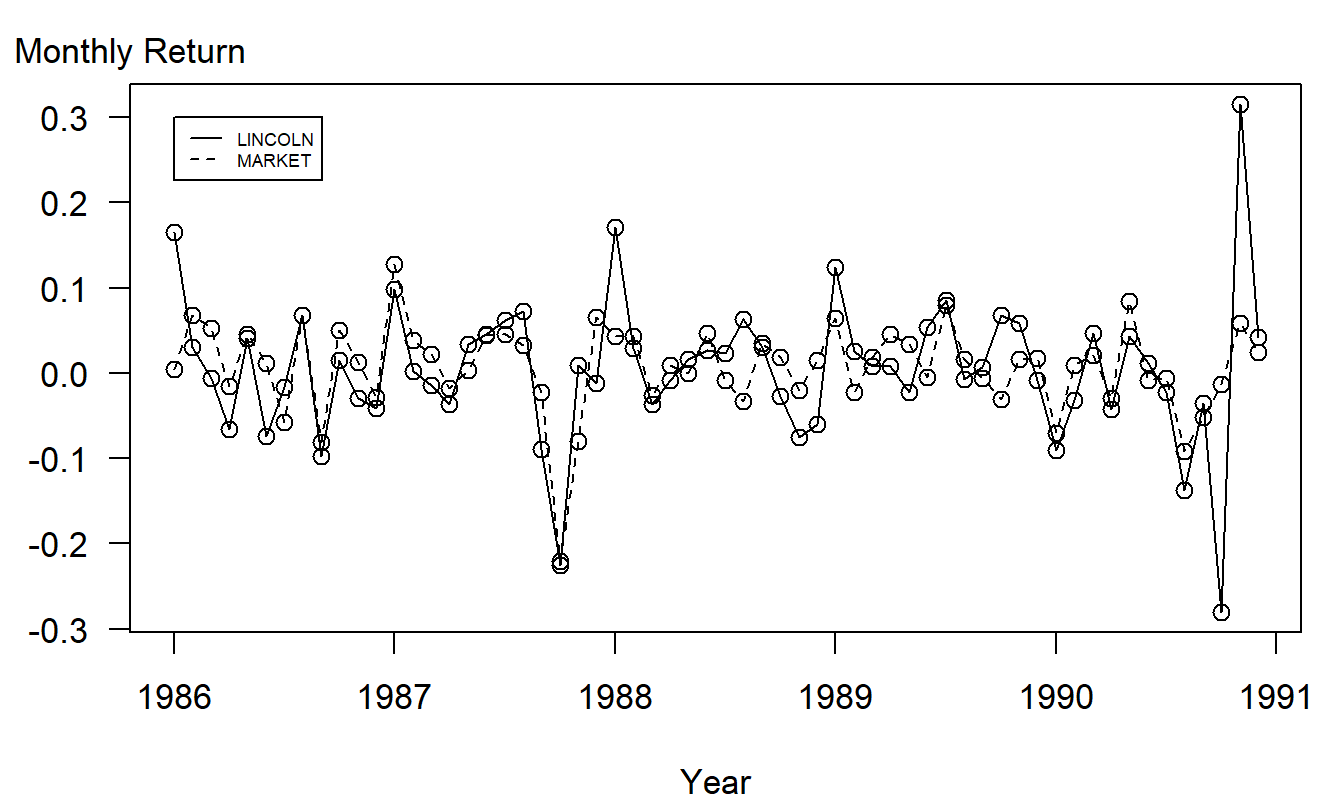

We next examine the data over time, as is given graphically in Figure 2.10. These are scatter plots of the returns versus time, called time series plots. In Figure 2.10, one can clearly see the smallest market return and a quick glance at the horizontal axis reveals that this unusual point is in October, 1987, the time of the well-known market crash.

Figure 2.10: Time series plot of returns from the Lincoln National Corporation and the market. There are 60 monthly returns over the period January, 1986 through December, 1990.

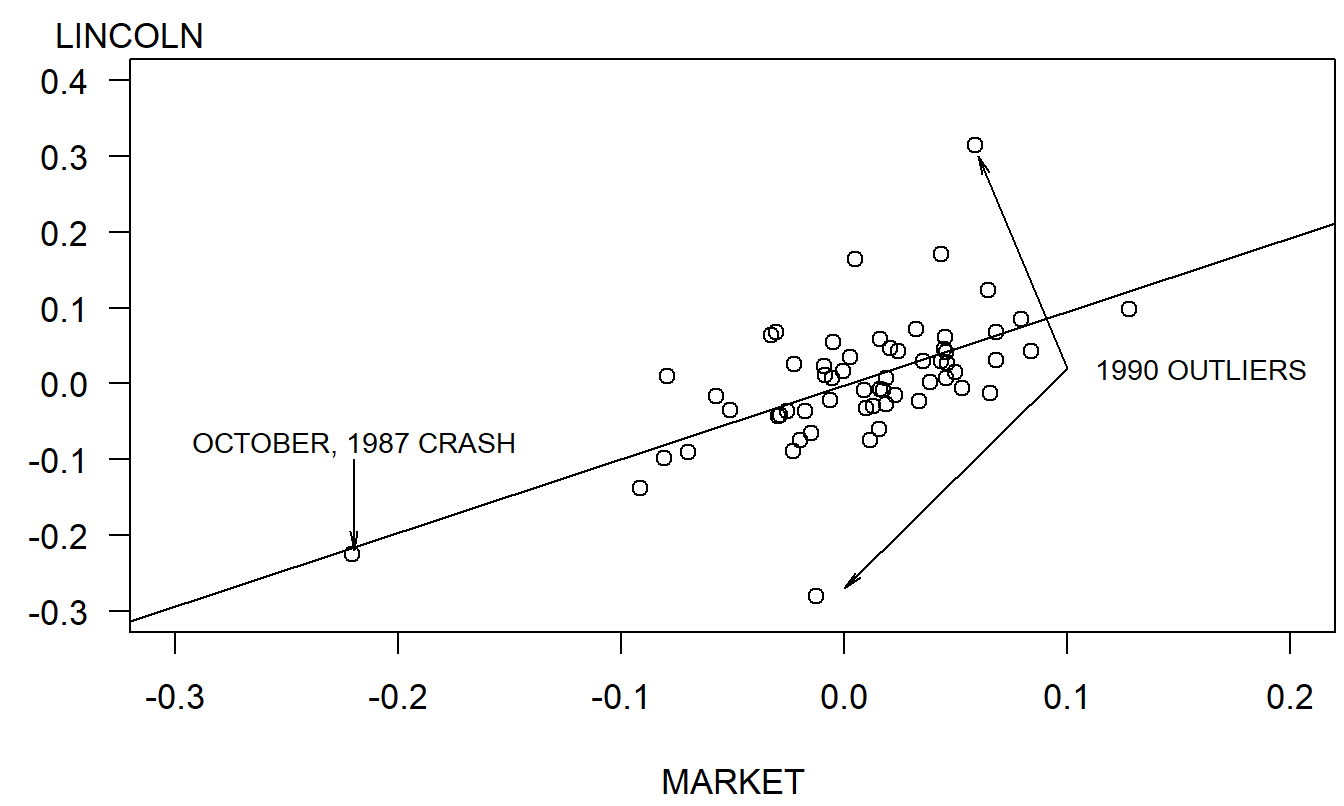

The scatter plot in Figure 2.11 graphically summarizes the relationship between Lincoln’s return and the return of the market. The market crash is clearly evident in Figure 2.11 and represents a high leverage point. With the regression line (described below) superimposed, the two outlying points that can be seen in Figure 2.10 are also evident. Despite these anomalies, the plot in Figure 2.11 does suggest that there is a linear relationship between Lincoln and market returns.

Figure 2.11: Scatterplot of Lincoln’s return versus the S&P 500 Index return. The regression line is superimposed, enabling us to identify the market crash and two outliers.

R Code to Produce Table 2.8 and Figures 2.10 and 2.11

Unusual Points

To summarize the relationship between the market and Lincoln’s return, a regression model was fit. The fitted regression is \[ \widehat{LINCOLN}=-0.00214+0.973 MARKET. \] The resulting estimated standard error, \(s\) = 0.0696 is lower than the standard deviation of Lincoln’s returns, \(s_y=0.0859\). Thus, the regression model explains some of the variability of Lincoln’s returns. Further, the \(t\)-statistic associated with the slope \(b_1\) turns out to be \(t(b_1)=5.64\), which is significantly large. One disappointing aspect is that the statistic \(R^2=35.4\%\) can be interpreted as saying that the market explains only a little over a third of the variability. Thus, even though the market is clearly an important determinant, as evidenced by the high \(t\)-statistic, it provides only a partial explanation of the performance of the Lincoln’s returns.

In the context of the market model, we may interpret the standard deviation of the market, \(s_x\), as non-diversifiable risk. Thus, the risk of a security can be decomposed into two components, the diversifiable component and the market component, which is non-diversifiable. The idea here is that by combining several securities we can create a portfolio of securities that, in most instances, will reduce the riskiness of our holdings when compared with a single security. Again, the rationale for holding a security is that we are compensated through higher expected returns by holding a security with higher riskiness. To quantify the relative riskiness, it is not hard to show that \[\begin{equation} s_y^2 = b_1^2 s_x^2 + s^2 \frac{n-2}{n-1}. \tag{2.8} \end{equation}\]

The riskiness of a security is due to the riskiness due to the market plus the riskiness due to a diversifiable component. Note that the riskiness due to the market component, \(s_x^2\), is larger for securities with larger slopes. For this reason, investors think of securities with slopes \(b_1\) greater than one as “aggressive” and slopes less than one as “defensive.”

Sensitivity Analysis

The above summary immediately raises two additional issues. First, what is the effect of the October, 1987 crash on the fitted regression equation? We know that unusual observations, such as the crash, may potentially influence the fit a great deal. To this end, the regression was re-run without the observation corresponding to the crash. The motivation for this is that the October 1987 crash represents a combination of highly unusual events (the interaction of several automated trading programs operated by the large stock brokerage houses) that we do not wish to represent using the same model as our other observations. Deleting this observation, the fitted regression is \[ \widehat{LINCOLN} = -0.00181 + 0.956 MARKET, \] with \(R^2=26.4\%\), \(t(b_1)=4.52\), \(s=0.0702\) and \(s_y=0.0811\). We interpret these statistics in the same fashion as the fitted model including the October 1987 crash. It is interesting to note, however, that the proportion of variability explained has actually decreased when excluding the influential point. This serves to illustrate an important point. High leverage points are often looked upon with dread by data analysts because they are, by definition, unlike other observations in the data set and require special attention. However, when fitting relationships among variables, they also represent an opportunity because they allow the data analyst to observe the relationship between variables over broader ranges than otherwise possible. The downside is that these relationships may be nonlinear or follow an entirely different pattern when compared to the relationships observed in the main portion of the data.

The second question raised by the regression analysis is what can be said about the unusual circumstances that gave rise to the unusual behavior of Lincoln’s returns in October and November of 1990. A useful feature of regression analysis is to identify and raise the question; it does not resolve it. Because the analysis clearly pinpoints two highly unusual points, it suggests to the data analyst to go back and ask some specific questions about the sources of the data. In this case, the answer is straightforward. In October of 1990, the Travelers’ Insurance Company, a competitor, announced that it would take a large write-off in their real estate portfolio. due to an unprecedented number of mortgage defaults. The market reacted quickly to this news, and investors assumed that other large stock life insurers would also soon announce large write-offs. Anticipating this news, investors tried to sell their portfolios of, for example, Lincoln’s stock, thus causing the price to plummet. However, it turned out that investors overreacted to this news and that Lincoln’s portfolio of real estate was indeed sound. Thus, prices quickly returned to their historical levels.

2.8 Illustrative Regression Computer Output

Computers and statistical software packages that perform specialized calculations play a vital role in modern-day statistical analyses. Inexpensive computing capabilities have allowed data analysts to focus on relationships of interest. Specifying models that are attractive merely for their computational simplicity is much less important now compared to times before the widespread availability of inexpensive computing. An important theme of this text is to focus on relationships of interest and to rely on widely available statistical software to estimate the models that we specify.

With any computer package, generally the most difficult parts of operating the package are the (i) input, (ii) using the commands and (iii) interpreting the output. You will find that most modern statistical software packages accept spreadsheet or text-based files, making input of data relatively easy. Personal computer statistical software packages have menu-driven command languages with easily accessible on-line help facilities. Once you decide what to do, finding the right commands is relatively easy.

This section provides guidance in interpreting the output of

statistical packages. Most statistical packages generate similar

output. Below, three examples of standard statistical software

packages, EXCEL, SAS and R are given. The annotation symbol

“[.]” marks a statistical quantity that is described in the

legend. Thus, this section provides a link between the notation used

in the text and output from some of the standard statistical

software packages.

EXCEL Output

Regression Statistics

Multiple R 0.886283[F]

R Square 0.785497[k]

Adjusted R Square 0.781028[l]

Standard Error 3791.758[j]

Observations 50[a]

ANOVA

df SS MS F Significance F

Regression 1[m] 2527165015 [p] 2527165015 [s] 175.773[u] 1.15757E-17[v]

Residual 48[n] 690116754.8[q] 14377432.39[t]

Total 49[o] 3217281770 [r]

Coefficients Standard Error t Stat P-value

Intercept 469.7036[b] 702.9061896[d] 0.668230846[f] 0.507187[h]

X Variable 1 0.647095[c] 0.048808085[e] 13.25794257[g] 1.16E-17[i]The SAS System

The REG Procedure

Dependent Variable: SALES

Analysis of Variance

Sum of Mean

Source DF Squares Square F Value Pr > F

Model 1[m] 2527165015[p] 2527165015[s] 175.77[u] <.0001[v]

Error 48[n] 690116755[q] 14377432[t]

Corrected Total 49[o] 3217281770[r]

Root MSE 3791.75848[j] R-Square 0.7855[k]

Dependent Mean 6494.82900[H] Adj R-Sq 0.7810[l]

Coeff Var 58.38119[I]

Parameter Estimates

Parameter Standard

Variable Label DF Estimate Error t Value Pr > |t|

Intercept Intercept 1 469.70360[b] 702.90619[d] 0.67[f] 0.5072[h]

POP POP 1 0.64709[c] 0.04881[e] 13.26[g] <.0001[i]R Output

Analysis of Variance Table

Response: SALES

Df Sum Sq Mean Sq F value Pr(>F)

POP 1[m] 2527165015[p] 2527165015[s] 175.77304[u] <2.22e-16[v]***

Residuals 48[n] 690116755[q] 14377432[t]

---

Call: lm(formula = SALES ~ POP)

Residuals:

Min 1Q Median 3Q Max

-6047 -1461 -670 486 18229

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 469.7036[b] 702.9062[d] 0.67[f] 0.51 [h]

POP 0.6471[c] 0.0488[e] 13.26[g] <2e-16 ***[i]

---

Signif. codes: 0 ?***? 0.001 ?**? 0.01 ?*? 0.05 ?.? 0.1 ? ? 1

Residual standard error: 3792[j] on 48[n] degrees of freedom

Multiple R-Squared: 0.785[k], Adjusted R-squared: 0.781[l]

F-statistic: 176[u] on 1[m] and 48[n] DF, p-value: <2e-16[v]Legend Annotation Definition, Symbol

[a] Number of observations \(n\).

[b] The estimated intercept \(b_0\).

[c] The estimated slope \(b_1\).

[d] The standard error of the intercept, \(se(b_0)\).

[e] The standard error of the slope, \(se(b_1)\).

[f] The \(t\)-ratio associated with the intercept, \(t(b_0) = b_0/se(b_0)\).

[g] The \(t\)-ratio associated with the slope, \(t(b_1) = b_1/se(b_1)\).

[h] The \(p\)-value associated with the intercept; here, \(p-value=Pr(|t_{n-2}|>|t(b_0)|)\), where \(t(b_0)\) is the realized value (0.67 here) and \(t_{n-2}\) has a \(t\)-distribution with \(df=n-2\).

[i] The \(p\)-value associated with the slope; here, \(p-value=Pr(|t_{n-2}|>|t(b_1)|)\), where \(t(b_1)\) is the realized value (13.26 here) and \(t_{n-2}\) has a \(t\)-distribution with \(df=n-2\).

[j] The residual standard deviation, \(s\).

[k] The coefficient of determination, \(R^2\).

[l] The coefficient of determination adjusted for degrees of freedom, \(R_{a}^2\). (This term will be defined in Chapter 3.)

[m] Degree of freedom for the regression component. This is 1 for one explanatory variable.

[n] Degree of freedom for the error component, \(n-2\), for regression with one explanatory variable.

[o] Total degrees of freedoms, \(n-1\).

[p] The regression sum of squares, \(Regression~SS\).

[q] The error sum of squares, \(Error~SS\).

[r] The total sum of squares, \(Total~SS\).

[s] The regression mean square, \(Regression~MS = Regression~SS/1\), for one explanatory variable.

[t] The error mean square, \(s^2=Error~MS = Error~SS/(n-2)\), for one explanatory variable.

[u] The \(F-ratio=(Regression~MS)/(Error~MS)\). (This term will be defined in Chapter 3.)

[v] The \(p\)-value associated with the \(F-ratio\). (This term will be defined in Chapter 3.)

[w] The observation number, \(i\).

[x] The value of the explanatory variable for the \(i\)th observation, \(x_i\).

[y] The response for the \(i\)th observation, \(y_i\).

[z] The fitted value for the \(i\)th observation, \(\widehat{y}_i\).

[A] The standard error of the fit, \(se(\widehat{y}_i)\).

[B] The residual for the \(i\)th observation, \(e_i\).

[C] The standardized residual for the \(i\)th observation, \(e_i/se(e_i)\). The standard error \(se(e_i)\) will be defined in Section 5.3.1.